VISIT STATE HEALTH COMPARE

VISIT STATE HEALTH COMPARE

Blog & News

Blewett, Lynn A.

Hest, Robert

Oregon Joins States Hoping to Stabilize Individual Market through Reinsurance Using 1332 Waivers

September 15, 2017:Update September 15, 2017: On August 31, Oregon submitted a 1332 Waiver Application to seek pass-through funding for its reinsurance proposal. $90 million in annual state funding for reinsurance plan is paid for through a 0.3% assessment levied on major medical premiums and through excess fund balances in two state programs. The state is seeking more than $30 million annually in federal pass-through funding. The reinsurance plan has a coinsurance rate of 50% and a cap of $1 million. The attachment point is to be determined.

On August 16, Oklahoma submitted its 1332 reinsurance proposal, called the Oklahoma Individual Health Insurance Market Stabilization Program (OMSP). The OMSP will have a broad corridor of $15,000 – $400,000 and will be largely funded with federal pass-through funding, with a smaller portion coming from a state assessment on health insurers.

UPDATE August 3, 2017: Minnesota’s Department of Commerce has released preliminary individual market premium increases with and without reinsurance. With state reinsurance, plans expect that 2018 premiums could be modestly higher (largest increase 11.4%) to modestly lower (largest decrease 14.5%) than 2017 premiums. Without state reinsurance, plans project much larger increases in 2018 premiums.

In addition, Oklahoma and New Hampshire recently released draft 1332 Waiver Applications to seek pass-through funding for state reinsurance proposals. Oklahoma’s 1332 waiver proposal includes reinsurance along with broader reforms to its individual market. The state is awaiting further actuarial analysis before determining its reinsurance plan’s corridor, coinsurance rate, and level of pass-through funding. Both Oklahoma’s and New Hampshire’s proposals are traditional reinsurance plans funded by assessments on health insurers. The table and text below has been updated accordingly.

UPDATE July 9, 2017: HHS approved Alaska's 1332 Waiver on July 7, 2017. The state was awarded $48.3 million in federal pass-through funding in 2018, and a total of $322 million over five years. The table below has been updated to reflect this development.

June 29, 2017: Minnesota, Alaska, and Iowa have each submitted 1332 State Innovation Waivers seeking federal funding of their state-based reinsurance proposals. Minnesota and Alaska, each of which entered their most recent legislative sessions with a budget surplus, have passed bipartisan legislation and provided initial state funding for their reinsurance plans; Iowa, which faced a budget shortfall of nearly $100 million, has not passed legislation or established state funding but submitted a 1332 waiver request that seeks federal funding for reinsurance along with significant changes to the state's Marketplace subsidy levels and eligibility.

The following table highlights key elements of the three 1332 reinsurance proposals along with the details of awarded funding, where applicable.

|

1332 STATE INNOVATION WAIVERS FOR STATE-BASED REINSURANCE

|

||||||

|---|---|---|---|---|---|---|

| Alaska Comprehensive Health Insurance Fund | Minnesota Premium Security Plan | Iowa 1332 Waiver Reinsurance Plan | Oklahoma Individual Health Insurance Market Stabilization Act | New Hampshire 1332 Waiver Reinsurance Plan | Oregon Reinsurance Program (ORP) | |

| REINSURANCE PROPOSAL | ||||||

| Reinsurance Type | Condition-specific reinsurance | Traditional reinsurance | Traditional reinsurance | Traditional reinsurance | Traditional reinsurance | Traditional reinsurance |

| Reinsurance Corridor | All claims from policyholders with one of 33 specific medical conditions | $50,000 – $250,000 | $100,000 – $300,000 | $15,000-$400,000 | $45,000 – $250,000 | TBD – $1,000,000 |

| Coinsurance Rate | 100% | 80% / 20% | 85% / 15% (Claims > $3 Million: 100%) |

80%/ 20^ | 40% / 60% | 50% / 50% |

| Legislation Enacted | HB 374, November 7, 2016 | HF 5, April 4, 2017 | No applicable state legislation |

HB 2406 |

HB 469 July 10, 2017 |

HB 2391 July 5, 2017 |

| 1332 STATE INNOVATION WAIVER | ||||||

| Approval Status |

Submitted December 29, 2016 |

Submitted May 5, 2017 | Submitted June 12, 2017 | Submitted August 16, 2017 | Draft waiver released for public comment July 19, 2017 | Submitted August 31, 2017 |

| State Funding | $55 million annually (51.6% of total) |

$271 million annually (61.9% - 66.3% of total) |

$0 (0% of total) |

$16 million in 2018 $230 million over five years (14.2% of total) |

$32 million annually (71.4% of total) | $90 milion in 2018 $1.1 billion over ten years (68.5% of total) |

| 1332 Funding Request | $51.6 million in pass-through funding (48.4% of total) |

$138 - $167 million in pass-through funding (33.7% - 38.1% of total) |

$80 million in pass-through funding for reinsurance (100% of total) |

$309 million in pass-through funding in 2018 $1,395 million over five years (85.8% of total) |

$12.8 million in pass-through funding for reinsurance (28.6% of total) | $35.66 million in 2018 $356.6 million over ten years (31.5% of total) |

| 1332 Funding Received | $48.3 million (2018) $332 million (2018-2022) |

|||||

| INDIVIDUAL MARKET | ||||||

| Marketplace Type 1 | Federally-facilitated Marketplace | State-based Marketplace | State-partnership Marketplace | Federally-facilitated Marketplace | Federally-facilitated Marketplace | State-based Marketplace with Federal Platform |

| Medicaid Expansion Status | Expanded Medicaid 2 | Expanded Medicaid 3 | Expanded Medicaid 4 | Did not expand Medicaid | Expanded Medicaid5 | Expanded Medicaid |

The reinsurance programs proposed in the 1332 Waivers are of two different designs. Iowa and Minnesota’s proposals are traditional reinsurance programs where claims in a specified corridor (e.g. $50,000–$250,000) are paid, minus a coinsurance rate; Alaska’s program is condition specific, with the state paying all claims for individuals with one or more of 33 specific conditions. Iowa’s proposal to cover 100 percent of claims above $3 million appears to be targeted at helping insurers pay the claims of an individual market enrollee whose treatment for a severe genetic disorder routinely generates more than $1 million per month in claims.

The letter from Secretary Price to state Governors earlier this spring suggested that states pursue reinsurance, and these are the first states out of the block. We will add details as the review process moves along. A key outcome will be whether CMS enforces their requirement that 1332 Waivers be authorized by state legislation as specified in the 1332 Waiver checklist issued May 11, 2017. (As noted above, Iowa’s 1332 Waiver was submitted by the state’s insurance commissioner and is not associated with any state legislation.)

1Kaiser Family Foundation. "State Health Insurance Marketplace Types, 2017."

2Expanded Medicaid September 1, 2015

3Minnesota also has MinnesotaCare, the Basic Health Program (BHP) for individuals 138-200% FPL.

4Expanded Medicaid with Section 1115 Waiver

5Expanded Medicaid with Section 1115 Waiver

Blog & News

2016 ACS: Public & Private Coverage Increased Nationally, State Story is Mixed

September 14, 2017:The U.S. Census Bureau released the full state files for the 2016 American Community Survey (ACS) today, including state-level information about health insurance coverage by coverage type.

National Coverage by Type, 2015-2016: Increases across the Board

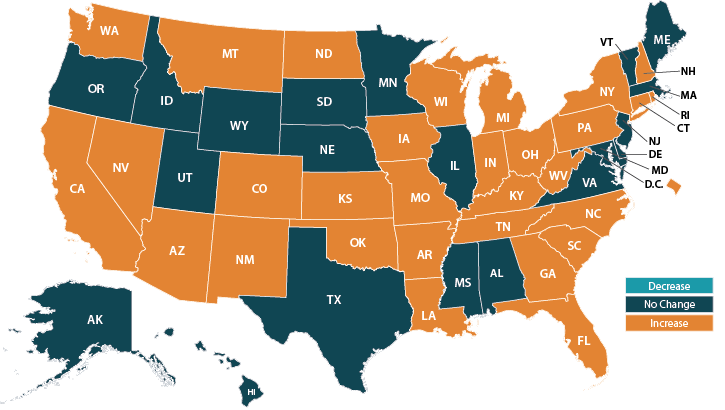

The ACS found a 0.8 percentage-point national increase in health insurance coverage between 2015 and 2016, from 90.6% to 91.4%. This increase was driven (as was the case last year) by increases in both public and private coverage: Public coverage grew from 34.7% in 2015 to 35.4% in 2016 (a 0.7 percentage-point increase), and private coverage grew from 67.5% to 67.8% (a 0.3 percentage-point increase). [1]

The national overall increase in insurance coverage in 2016 was mirrored by significant overall coverage increases in 39 states (with no state seeing a significant decrease in coverage overall). However, there was variation among states in the extent to which there were coverage changes in rates of public and private coverage in particular, and in whether these changes represented increases or decreases.[2]

Public Coverage Rates by State, All Ages, 2015 to 2016: Changes Similar to Last Year

- Public coverage increased significantly in 29 states and the District of Columbia

- 21 states saw no significant changes in public coverage

- No state saw a statistically significant decrease in public coverage

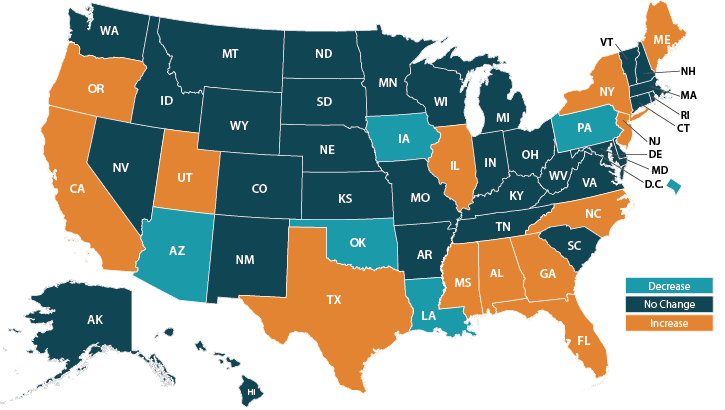

Private Coverage Rates by State, All Ages, 2015 to 2016: Fewer Increases, More Decreases than Last Year

- Private coverage increased significantly in 13 states, down from 30 states and the District of Columbia in 2015

- 32 states experienced no significant changes in private coverage

- Five states and the District of Columbia experienced significant decreases in private coverage; this contrasts with 2015, when no state saw significant private coverage decreases

Public and Private Coverage Rates by State, All Ages, 2016: State Variation Continued

State variation is seen not only in the prevalence and direction of public and private coverage changes between 2015 and 2016 but also in levels of public and private coverage when looking at the 2016 estimates on their own.

- West Virginia had the highest rate of public coverage in 2016, at 48.4%

- Utah had the lowest rate of public coverage in 2016 (as in 2015), at 21.5%

- North Dakota reported the highest rate of private coverage in 2016 (as in 2015), at 80.5%

- New Mexico (as in 2015) had the lowest rate of private coverage in 2016, at 55.1%.

Access the full 2016 ACS 1-year tables on American FactFinder.

More to Come

Stay tuned for more granular details about insurance coverage changes in the states from 2015 to 2016 via customized SHADAC tables examining coverage at the state and county level.

Related Reading

2016 ACS: Uninsured Rate Fell Nationally and in 39 States

SHADAC Blog, September 12, 2016

Census Bureau Experts Will Share Insights during September 19th Webinar

On Tuesday, September 19th, SHADAC will host a webinar to examine the new 2016 ACS and CPS estimates, with technical insight provided by researchers from SHADAC and from the U.S. Census Bureau, which administers both surveys.

Speakers will discuss the new national and state estimates, and attendees will learn:

- When to use which estimates from which survey

- How to access the estimates via Census reports and American FactFinder

- How to access state-level estimates from the ACS using SHADAC tables

Attendees will have an opportunity to ask questions after the speaker presentations.

[1] Sum of public and private coverage estimates exceeds 100% because survey respondents may report more than one type of coverage.

[2] Private coverage includes individually-purchased and employer-sponsored coverage.

Blog & News

2016 ACS: Uninsured Rate Fell Nationally and in 39 States

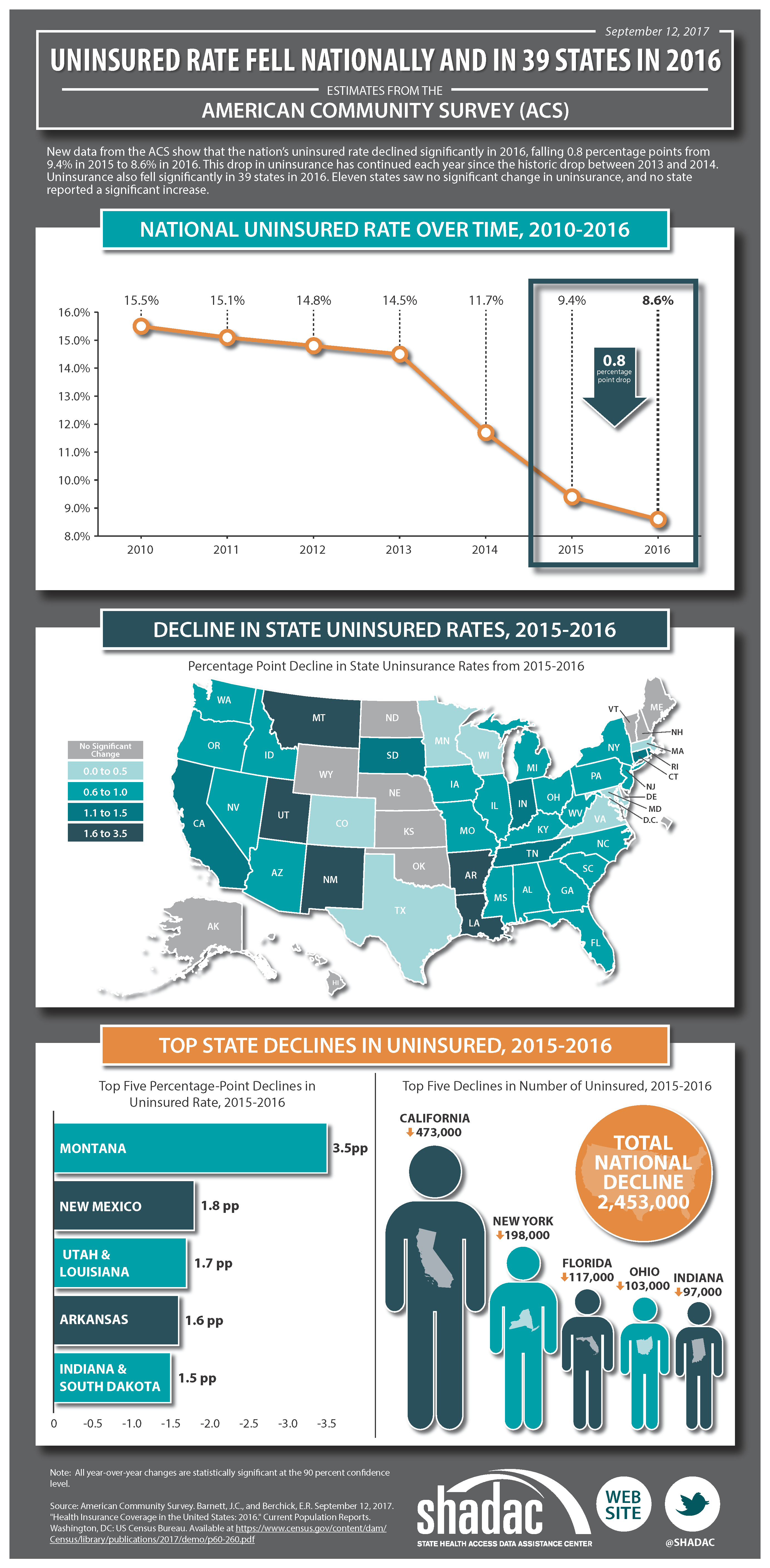

September 12, 2017: New health insurance coverage estimates from the American Community Survey (ACS) show that there was a statistically significant decline in the national uninsured rate between 2015 and 2016. Uninsurance also declined significantly in 39 states between 2015 and 2016, with year-over-year changes and 2016 rates varying widely between states.

New health insurance coverage estimates from the American Community Survey (ACS) show that there was a statistically significant decline in the national uninsured rate between 2015 and 2016. Uninsurance also declined significantly in 39 states between 2015 and 2016, with year-over-year changes and 2016 rates varying widely between states.

Uninsurance from 2015 to 2016

- The national uninsurance rate fell from 9.4% in 2015 to 8.6% in 2016 (a 0.8 percentage-point drop), with almost 2.5 million fewer uninsured Americans in 2016. This drop in uninsurance has continued every year since the historic drop between 2013 and 2014.

- Among the 39 states that saw significant declines in their uninsured rates from 2015 to 2016, Montana saw the largest percentage-point decrease, from 11.6% to 8.1% (-3.5pp), and Massachusetts saw the smallest decrease, from 2.8% to 2.5% (-0.3pp).

- Eleven states (Alaska, Delaware, Hawaii, Kansas, Maine, Nebraska, New Hampshire, North Dakota, Oklahoma, Vermont, and Wyoming) and the District of Columbia saw no statistically significant change in uninsurance between 2015 and 2016. No state saw a statistically significant increase in uninsurance during this time period.

Uninsurance Levels in 2016

- Texas continues to have the highest uninsured in 2016, at 16.6%, although this was a decrease from 17.1% in 2015.

- The lowest 2016 uninsured rate was 2.5% in Massachusetts. This was also (as noted above) a decrease from 2015, when the state’s uninsured rate was 2.8%.

- Among Medicaid expansion states[1], the average uninsured rate in 2016 was 6.5%, and individual state uninsurance rates ranged from a low of 2.5% in Massachusetts to a high of 14.0% in Alaska.

- Among non-expansion states, the average uninsured rate in 2016 was 11.7%, and individual state uninsurance rates ranged from a low of 5.3% in Wisconsin to a high of 16.6% in Texas.

See our infographic illustrating uninsurance in Minnesota.

The ACS Estimates in Context

The findings from the 2016 ACS are consistent with estimates from the Current Population Survey (CPS), which were also released today. The CPS found that the percentage of all people who were uninsured for the entire calendar year fell 0.3 percentage points nationwide, from 9.1% in 2015 to 8.8% in 2016.

Census Bureau Experts Will Share Insights during September 19th Webinar

On Tuesday, September 19th, SHADAC will host a webinar to examine the new 2016 ACS and CPS estimates, with technical insight provided by researchers from SHADAC and from the U.S. Census Bureau, which administers both surveys.

Speakers will discuss the new national and state estimates, and attendees will learn:

- When to use which estimates from which survey

- How to access the estimates via Census reports and American FactFinder

- How to access state-level estimates from the ACS using SHADAC tables

Attendees will have an opportunity to ask questions after the speaker presentations.

[1] Medicaid expansion status as of January 1, 2016.

Blog & News

September 19th ACS & CPS Data Release Webinar

September 8, 2017:Webinar

New Coverage Data from the ACS and CPS: An Annual Conversation with Census Bureau Experts

Date: September 19, 2017

Time: 12:00 p.m. Central (1:00 p.m. ET / 11:00 a.m. MT / 10:00 a.m. PT)

Join us on September 19th as we look at new health insurance coverage estimates from two key, large-scale federal data sources: The American Community Survey (ACS) and the Current Population Survey (CPS). The U.S. Census Bureau is releasing 2016 data from these annual surveys on September 12th and 14th, providing a detailed picture of coverage at the national and state level under three years of ACA implementation while also providing historical trend information for context.

This webinar will examine the new 2016 ACS and CPS coverage estimates with technical insight from SHADAC researchers and from experts at the Census Bureau.

Attendees will learn about:

- The new 2016 national and state coverage estimates

- When to use which estimates from which survey

- How to access the estimates via Census reports and American FactFinder

- How to access state-level estimates from the ACS using SHADAC tables

SHADAC researchers and Census experts will answer questions from attendees after the presentation.

Blog & News

Trends in Employer-Sponsored Insurance, 2012-2016: Deductible Increases Offset Slowdown in Premium Growth

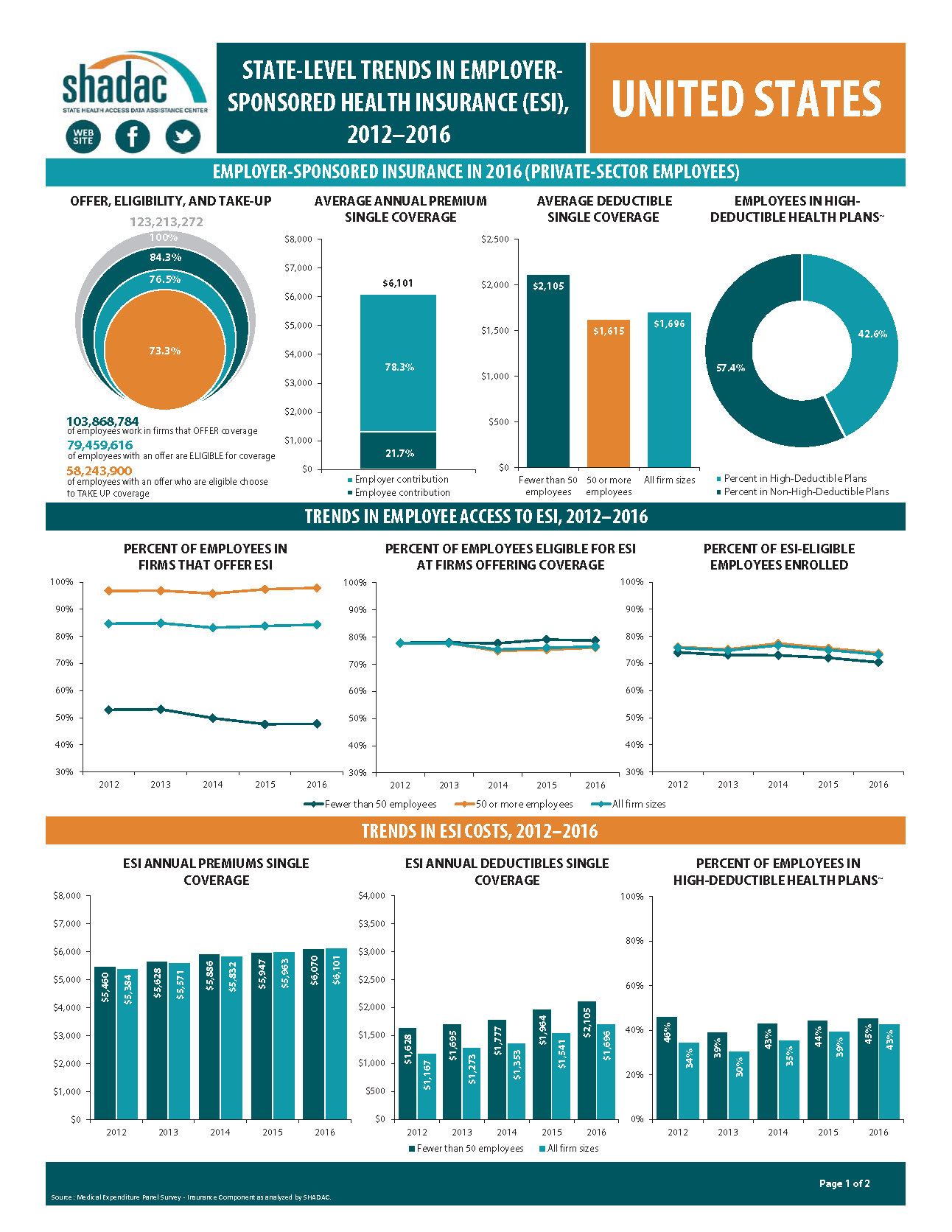

September 6, 2017:A new analysis from SHADAC highlights the experiences of private sector workers with employer-sponsored insurance (ESI) from 2012 through 2016 at the national level and in the states.

Key Findings

- Nationally, the percentage of employers offering health insurance coverage was unchanged from 2015 to 2016, as was the percentage of workers eligible for ESI offered to them.

- Changes in offer rates from 2015 to 2016 varied by firm size: Offer rates stabilized among small firms but increased among large firms.

- Nationally, 73.3 percent of eligible workers were enrolled in ESI in 2016, down 1.7 percentage points (pp) from 2015.

- Premium increases have continued, but the growth rate of premiums remained stable from 2015 to 2016.

- Slowed premium growth from 2015 to 2016 was offset by a 10.1 percent ($155) increase in average deductibles during this time period.

- The proportion of workers enrolled in high-deductible health plans nationwide grew significantly from 2015 to 2016, reaching 42.6 percent (a 3.2pp increase).

- State variation in access to and enrollment in ESI plans, along with ESI cost, continued.

The Takeaway

Employer-sponsored insurance continues to be the backbone of the insurance coverage system in the United States, covering more than half the population, but we are seeing a decline in the financial protection provided by employer coverage.

SHADAC Deputy Director Elizabeth Lukanen noted, “SHADAC’s analysis shows that while the number of workers with employer-sponsored coverage isn’t changing much over time, the value of their coverage is eroding, as employees shoulder increasingly higher deductibles.”

And, with the dominant role of employer coverage in the broader coverage landscape, it’s important to note that even small changes in the value of employer coverage affect a significant number of people.

Explore the Analysis

The following products present findings from this analysis:

- Summary chartbook highlighting key findings on levels of, and trends in, employee access to and take up of ESI coverage as well as average ESI premiums and deductibles

- Two-page profiles of ESI for each state

- 50-state interactive map showing levels of, and changes in, worker enrollment in high-deductible health plans in 2016, with links to state profile pages

- 50-state comparison tables

About the Data

This analysis uses data from the Medical Expenditure Panel Survey-Insurance Component (MEPS-IC).