VISIT STATE HEALTH COMPARE

VISIT STATE HEALTH COMPARE

Blog & News

Minnesota and U.S. Uninsurance Rates Grew in Years Leading up to Pandemic

October 27, 2020:Children’s uninsurance rate held steady recently, while non-elderly adults’ rate increased in 2019

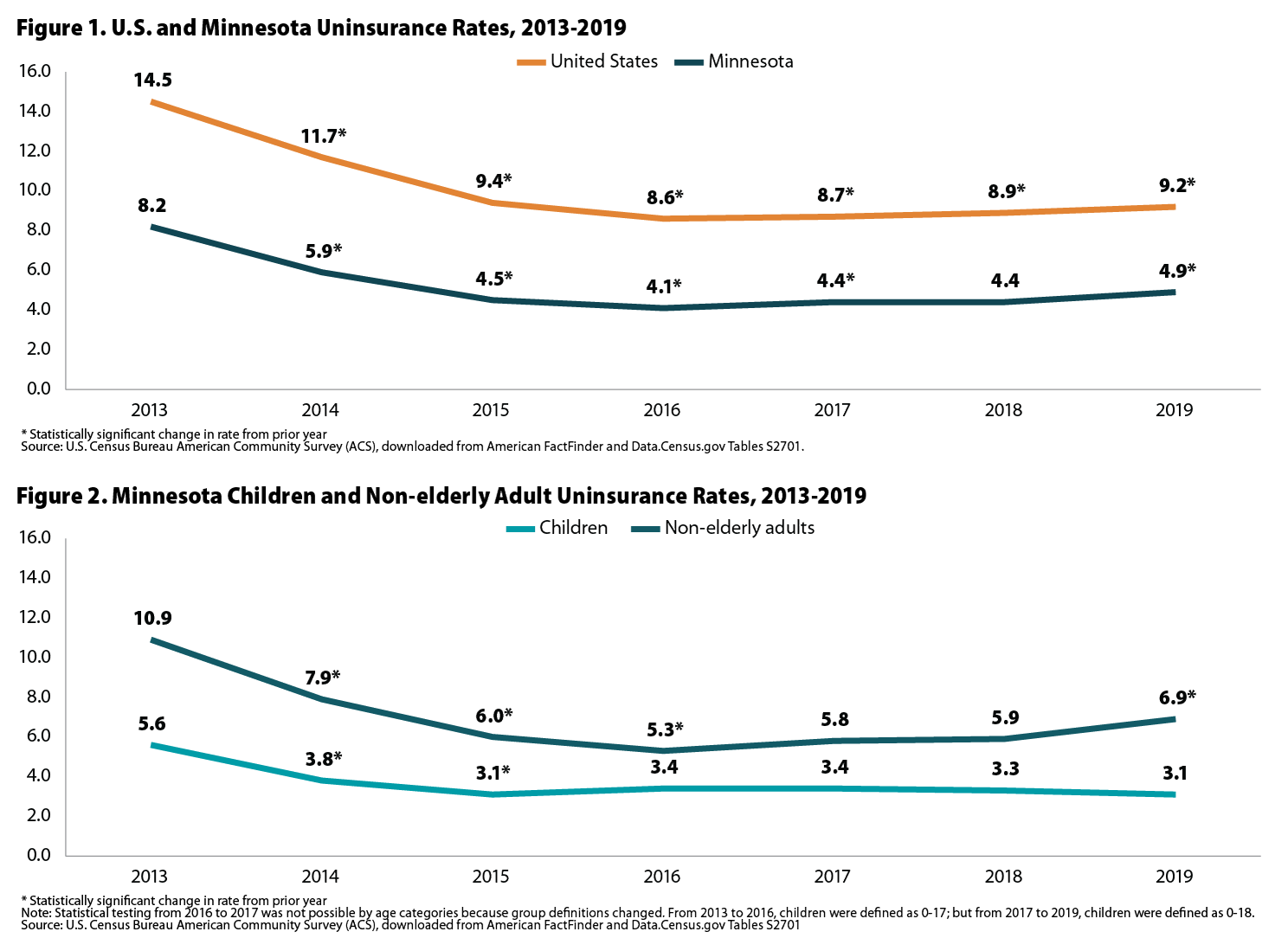

For the third consecutive year, the United States' uninsurance rate increased significantly, reaching 9.2 percent in 2019, or roughly 27.9 million people. The uninsurance rate in Minnesota also increased significantly to 4.9 percent in 2019—a total of more than 270,000 people. While those increases are troubling by themselves, uninsurance rates are likely to grow even further in 2020 due to the COVID-19 pandemic and ensuing recession, which triggered historic job losses and could further cause hundreds of thousands of Minnesotans—and tens of millions across the U.S.—to lose coverage.1

For the third consecutive year, the United States' uninsurance rate increased significantly, reaching 9.2 percent in 2019, or roughly 27.9 million people. The uninsurance rate in Minnesota also increased significantly to 4.9 percent in 2019—a total of more than 270,000 people. While those increases are troubling by themselves, uninsurance rates are likely to grow even further in 2020 due to the COVID-19 pandemic and ensuing recession, which triggered historic job losses and could further cause hundreds of thousands of Minnesotans—and tens of millions across the U.S.—to lose coverage.1

Successes and Reversals in the ACA’s Coverage Expansion

Following years of growing U.S. uninsurance rates, the passage of the Affordable Care Act (ACA) in 2010 was designed to expand health insurance coverage to millions of Americans through various reforms, including the expansion of Medicaid eligibility to low-income adults, and the creation of health insurance marketplaces and tax subsidies to make individual market coverage more affordable for people with moderate incomes.

The first year of the ACA’s coverage expansion provisions saw historic declines in U.S. uninsurance rates, dropping significantly from 14.5 percent in 2013 to 11.7 percent in 2014 (Figure 1). In the following years of 2015 and 2016, U.S. uninsurance rates declined further still, bottoming out at 8.6 percent in 2016. At the same time, Minnesota’s uninsurance rate was cut in half—declining from 8.2 percent in 2013 to 4.1 percent by 2016.

Figure 1. U.S. and Minnesota Uninsurance Rates, 2013-2019

Beginning in 2017, however, uninsurance rates began to creep back up. In the U.S., uninsurance rates increased significantly in 2017, 2018, and 2019, when they reached 9.2 percent. Minnesota uninsurance rates also grew significantly in 2017 and 2019, when they reached 4.9 percent.

In Minnesota, the increases in uninsurance appear to be driven primarily by non-elderly adults. The uninsurance rate for adults age 19-64 increased significantly between 2018 and 2019, from 5.9 percent to 6.9 percent—the second-highest recorded rate since implementation of the ACA (Figure 2).2 However, the uninsurance rate for children in Minnesota remained statistically unchanged from 2018 to 2019. In fact, the 2019 uninsurance rate of 3.1 percent for Minnesota children was the lowest since implementation of the ACA (tied with the 3.1 percent rate in 2015).

Figure 2. Minnesota Children and Non-elderly Adult Uninsurance Rates, 2013-2019

Even with the overall increase in uninsurance, Minnesota continued to have one of the lowest rates in the U.S.—lower than all but four other states (Massachusetts, Rhode Island, Hawaii, and Vermont) and the District of Columbia. The lowest 2019 state uninsurance rate was 3.0 percent in Massachusetts, while the highest was 18.4 percent in Texas.

Generally, states such as Minnesota that have taken up the ACA’s option to expand their Medicaid programs tend to have lower uninsurance rates, while states that haven’t expanded their Medicaid programs tend to have higher uninsurance rates. For instance, each of the earlier mentioned states with the lowest uninsurance rates (DC, HI, MA, MN RI, VT) has expanded its Medicaid program, while none of the states with the five highest uninsurance rates (Florida, Georgia, Mississippi, Oklahoma, and Texas) has expanded its Medicaid program.

The Pandemic’s Uninsurance Perils

Though definitive estimates of the impact of the pandemic on health insurance coverage won’t be available until federal survey data are released in late 2021, it’s all but certain that 2020 will show a significant increase in uninsurance rates nationally and in many states. While the share of Americans who get health insurance through an employer has declined over time, employer-sponsored insurance (ESI) remains the backbone of the U.S. health insurance system, with a majority of the U.S. population getting their insurance through ESI (52.0 percent in 2018).3

The historically massive job losses caused by the pandemic and efforts to contain the outbreak are estimated to have caused millions of people to lose their ESI in 2020. Some of those people may regain ESI coverage, through a replacement job or as a dependent on a spouse or parent’s plan. Others may obtain individual market coverage through health insurance marketplaces, perhaps with the assistance of ACA premium subsidies.

In Minnesota and other states that took up the ACA’s Medicaid expansion provision, many low-income people who have lost ESI will be able to rely on that public insurance program as a safety net. However, Medicaid coverage will not be an option for most adults who lost ESI in the 12 states that have yet to expand their Medicaid programs to childless adults. For that reason, those states that have yet to expand Medicaid may see larger increases in uninsurance as a result of the pandemic.

1 Golberstein, E., Abraham, J.M., Blewett, L.A., Fried, B., Hest, R., & Lukanen, E. (2020). Estimates of the Impact of COVID-19 on Disruptions and Potential Loss of Employer-Sponsored Health Insurance (ESI) [PDF file]. https://www.shadac.org/publications/COVID-19-MNHealth-Insurance-Model

2 From 2013 to 2016, non-elderly adults were defined as age 18-64, but from 2017 to 2019, they are defined as 19-64, so statistical testing of annual changes in rates was not possible for the subcategories of children and non-elderly adults between 2016 and 2017.

3 State Health Compare. Health Insurance Coverage Type: 2008-2018 [Data set]. State Health Access Data Assistance Center. http://statehealthcompare.shadac.org/trend/11/health-insurance-coverage-type-by-total#0/1/86/1,2,3,4,5,6,7,8,15,24,25/21

Publication

Using 1115 Waivers to Fund State Uncompensated Care Pools

What is an Uncompensated Care Pool?

Uncompensated care pools (UC pools, or UCPs) are one strategy used by states in order to fund care for the uninsured and the underinsured. The pools are primarily used to pay providers for a portion of the free care they provide, thereby ensuring access to critical inpatient hospital and other provider services. UC pools, also called “Low Income Pools,” leverage 1115 Medicaid demonstration waiver authority to fund hospitals and health systems that:

- Care for a large number of uninsured patients,

- Provide a disproportionate amount of charity care,

- Have incurred "bad debt" from unpaid bills, and/or

- Serve a disproportionately large number of Medicaid beneficiaries whose care is reimbursed at a lower rate than privately insured individuals.

This brief provides an overview of the seven states that use Medicaid 1115 demonstration waivers to fund their Uncompensated Care: California, Florida, Kansas, Massachusetts, New Mexico, Tennessee, and Texas. We also include information on two states—Arizona and Hawaii—with recently expired 1115 waivers that formerly were used to fund UC pools.

Publication

Comparing Federal Government Surveys That Count the Uninsured: 2020

With the release of new insurance coverage estimates from surveys conducted by the U.S. Census Bureau, the Agency for Healthcare Research and Quality (AHRQ), and the Centers for Disease Control and Prevention (CDC), SHADAC has updated our annual “Comparing Federal Government Surveys that Count the Uninsured” brief.

With the release of new insurance coverage estimates from surveys conducted by the U.S. Census Bureau, the Agency for Healthcare Research and Quality (AHRQ), and the Centers for Disease Control and Prevention (CDC), SHADAC has updated our annual “Comparing Federal Government Surveys that Count the Uninsured” brief.

The brief provides an annual update to comparisons of uninsurance estimates from four federal surveys:

- The American Community Survey (ACS)

- The Current Population Survey (CPS)

- The Medical Expenditure Panel Survey - Household Component (MEPS-HC)

- The National Health Interview Survey (NHIS)

In this brief, SHADAC presents current and historical national estimates of uninsurance along with the most recent available state-level estimates from these surveys. We also discuss the main reasons for variation in the estimates across the different surveys as well as possible reasons for incomparability of estimates across and within the surveys.

Download a PDF of the Comparing Federal Government Surveys Brief.

Last year’s brief with data from 2019, and certain 2018 data, can be accessed here.

Blog & News

New Subsidized Marketplace Data and Other Data Tables Now Available from the 2019 American Community Survey (ACS)

September 23, 2020:The U.S. Census Bureau recently released 2019 estimates of income, poverty, and health insurance coverage from both the Current Population Survey Annual Social and Economic Supplement (CPS ASEC) and the American Community Survey (ACS).

Along with the new estimates, several new data sets and features from the surveys are also now available for this year, including new estimates of subsidized marketplace insurance coverage, which is the main subject of this post.

New Data

In 2019, for the first time, the American Community Survey (ACS) asked respondents if they or a family member received a “tax credit or subsidy based on family income” to help pay for their coverage.1 These subsidies are only available through the Affordable Care Act (ACA) marketplaces for individuals who are eligible based on their family income. By adding this question, researchers at the Census Bureau and other data users are now able to create estimates for the number and percent of the population who receive subsidized ACA marketplace coverage.

As part of a high-level analysis, SHADAC researchers found that at the national level, approximately 1.6% of the civilian noninstitutionalized population reported having subsidized marketplace coverage—representing nearly 5.3 million individuals.

Across the states, rates of subsidized marketplace coverage ranged significantly from a low of 0.7% in West Virginia and D.C. to a high of 3.4% in Florida and Utah.

The five states with the largest populations of individuals with subsidized marketplace coverage were California, Florida New York, North Carolina, and Texas. More than 40% of total marketplace enrollees lived in one of these five states, and of that subsection of enrollees, nearly 3 in 5 lived in either California or Florida.

Eleven states (Florida, Idaho, Maine, Montana, Nebraska, North Carolina, South Carolina, South Dakota, Utah, Wisconsin, and Wyoming) had rates of subsidized marketplace coverage that were significantly higher than the national rate in 2019. Of these states, only Montana and Maine had implemented Medicaid expansion for the majority of 2019, which expands the portion of the population eligible for ACA subsidies. (Montana implemented Medicaid expansion as of January 1, 2019, and Maine implemented expansion on January 10, 2019.)

Twenty states (Alaska, Arizona, Arkansas, Connecticut, Delaware, Hawaii, Iowa, Illinois, Indiana, Kentucky, Louisiana, Massachusetts, Maryland, Minnesota, Mississippi, New Mexico, New York, Ohio, Washington, and West Virginia) and D.C. had rates of subsidized marketplace coverage that were significantly lower than the national rate in 2019. Of these 20 states and D.C., only Mississippi had chosen not to expand Medicaid as of January 1, 2019.

Nineteen states had rates of subsidized marketplace coverage that were not statistically different from the national rate.

New Data Tables and Geographic Breakdowns

Along with the new question and corresponding data table on subsidized coverage discussed above, other new data tables available from the ACS this year include:

- Population: a new table on place of birth shows the year of entry among the foreign-born population for the nine largest country of birth groups. Estimates are divided between year of entry before 2010 and year of entry beginning 2010 and later.

- Households and Families: two new tables provide information regarding (1) couples who live together with biological children, stepchildren, or adopted children of the main householder who are under 18 and have not been married; and (2) married couples, cohabiting couples, and single householders (male or female) with no spouse or partner present who also live with either relatives or their own children under 18.

- Quality Measure: this new table provides the unweighted total population sample for the nation, states, counties, and places.

Extensive modifications have also been made to existing ACS data tables, a full listing of which can be found here.

In addition to data table changes, the Census Bureau has also created an updated posting regarding geographic entities of varying sizes and designations (cities, towns, townships, school districts, Native American reservations, etc.) that have either come into existence, been absorbed into other entities, or have been dissolved in 2019. A full listing of all new, modified, or removed geographic breakdowns used for the 2019 ACS estimates can be found here.

Related Materials:

- 2019 ACS: Rising National Uninsured Rate Echoed Across 19 States; Virginia Only State to See Decrease (Infographics)

- 2019 ACS: Insurance Coverage Overall Fell Nationwide and among the States, with Private and Public Coverage Declines Seen at the State Level

- 2019 ACS Tables: State and County Uninsured Rates, with Comparison Year 2018

Note: All differences described here are significant at the 90% confidence level

Reference:

1 U.S. Census Bureau. (2018, August 2.) The American Community Survey: Questionnaire. Retrieved from https://www2.census.gov/programs-surveys/acs/methodology/questionnaires/2019/quest19.pdf

Blog & News

September 23rd Webinar - An Annual Conversation with the U.S. Census Bureau: 2019 Health Insurance Coverage Data from the American Community Survey (ACS) & Current Population Survey (CPS)

September 4, 2020:On Wednesday, September 23, 2020, SHADAC researchers and U.S. Census Bureau experts held a webinar that examined the new 2019 health insurance coverage data at both the national and the state level, as well as by coverage type, from both the American Community Survey (ACS) and the Current Population Survey Annual Social and Economic Supplement (CPS ASEC).

In addition to further details on important health insurance coverage data and trends,

webinar attendees learned about:

- When to use which estimates from which survey

- How to access the estimates via Census reports and Census data site: data.census.gov

- How to access state-level estimates from the ACS using SHADAC tables

Panelists on this webinar included:

Lynn Blewett, PhD - the founding Director of SHADAC, as well as a Professor in the Division of Health Policy and Management at the University of Minnesota, School of Public Health, where she teaches graduate courses on the U.S. health care system and international health systems. Dr. Blewett has a committed history in working and researching health policy, access to care, Medicaid coverage, and payment policy with experience at both the state and national levels. She has expertise in leading applied policy research, directing research with diverse funding, analyzing state and federal data resources and translating research to inform health policy. Her health policy experience includes legislative work for the U.S. Senate and state policy work as Director of the Health Economics Program for the Minnesota Department of Health. Dr. Blewett holds a Ph.D. and a master's in Public Affairs from the University of Minnesota, and a B.A. from the University of Wisconsin at Madison.

Lynn Blewett, PhD - the founding Director of SHADAC, as well as a Professor in the Division of Health Policy and Management at the University of Minnesota, School of Public Health, where she teaches graduate courses on the U.S. health care system and international health systems. Dr. Blewett has a committed history in working and researching health policy, access to care, Medicaid coverage, and payment policy with experience at both the state and national levels. She has expertise in leading applied policy research, directing research with diverse funding, analyzing state and federal data resources and translating research to inform health policy. Her health policy experience includes legislative work for the U.S. Senate and state policy work as Director of the Health Economics Program for the Minnesota Department of Health. Dr. Blewett holds a Ph.D. and a master's in Public Affairs from the University of Minnesota, and a B.A. from the University of Wisconsin at Madison.

Laryssa Mykyta, PhD - the chief of the Health and Disability Statistics Branch in the Social, Economic and Housing Statistics Division at the U.S. Census Bureau. The Health and Disability Statistics Branch is primarily responsible for analyzing and publishing data collected on health insurance coverage, health status and health care utilization, and disability. These data are collected in the Current Population Survey Annual Social and Economic Supplement, the American Community Survey, and the Survey of Income and Program Participation. Her research interests focus on how changing economic conditions influence health and well-being. Ms. Mykyta was previously an assistant professor in sociology and director of the Center for Survey Research and Policy Analysis at the University of Texas Rio Grande Valley. Ms. Mykyta received her doctorate in sociology and demography from the University of Pennsylvania.

Laryssa Mykyta, PhD - the chief of the Health and Disability Statistics Branch in the Social, Economic and Housing Statistics Division at the U.S. Census Bureau. The Health and Disability Statistics Branch is primarily responsible for analyzing and publishing data collected on health insurance coverage, health status and health care utilization, and disability. These data are collected in the Current Population Survey Annual Social and Economic Supplement, the American Community Survey, and the Survey of Income and Program Participation. Her research interests focus on how changing economic conditions influence health and well-being. Ms. Mykyta was previously an assistant professor in sociology and director of the Center for Survey Research and Policy Analysis at the University of Texas Rio Grande Valley. Ms. Mykyta received her doctorate in sociology and demography from the University of Pennsylvania.

Katherine Keisler-Starkey, PhD - an Economist and Survey Statistician at the U.S. Census Bureau. Ms. Keisler-Starkey's research interests focus on Applied Microeconomics, including Health Economics, Public Finance, and Labor Statistics. Ms. Keisler-Starkey received a Ph.D in Economics, a Bachelor of Science degree in Statistics, and a Bachelor of Arts degree in Economics from the University of Texas at Austin.

Katherine Keisler-Starkey, PhD - an Economist and Survey Statistician at the U.S. Census Bureau. Ms. Keisler-Starkey's research interests focus on Applied Microeconomics, including Health Economics, Public Finance, and Labor Statistics. Ms. Keisler-Starkey received a Ph.D in Economics, a Bachelor of Science degree in Statistics, and a Bachelor of Arts degree in Economics from the University of Texas at Austin.

Robert Hest, MPP - manages SHADAC’s State Health Compare website, coordinating data processing, quality assurance, dissemination and documentation of data used on the cite. Robert also works on SHADAC’s Minnesota Long-term Care Projection Model (MN-LPM), which projects future long-term care utilization and spending among older adults in Minnesota. In addition, Mr. Hest leads a project tracking and analyzing 1332 State Innovation Waivers for State-Based Reinsurance programs. Before joining the SHADAC staff as a Research Fellow in October 2017, Robert worked at SHADAC as a Graduate Research Assistant. He earned his Master of Public Policy from the Humphrey School of Public Affairs with an emphasis in Policy Analysis, and he received his Bachelor of Arts from Carleton College in Political Science.

Robert Hest, MPP - manages SHADAC’s State Health Compare website, coordinating data processing, quality assurance, dissemination and documentation of data used on the cite. Robert also works on SHADAC’s Minnesota Long-term Care Projection Model (MN-LPM), which projects future long-term care utilization and spending among older adults in Minnesota. In addition, Mr. Hest leads a project tracking and analyzing 1332 State Innovation Waivers for State-Based Reinsurance programs. Before joining the SHADAC staff as a Research Fellow in October 2017, Robert worked at SHADAC as a Graduate Research Assistant. He earned his Master of Public Policy from the Humphrey School of Public Affairs with an emphasis in Policy Analysis, and he received his Bachelor of Arts from Carleton College in Political Science.

A recording of the webinar is available to view and download at the top of this page, and slides and a transcript are also available for download.

Related Resources

2019 ACS Tables: State and County Uninsured Rates, with Comparison Year 2018