VISIT STATE HEALTH COMPARE

VISIT STATE HEALTH COMPARE

Publication

May 23rd Virtual Tour of State Health Compare: A New Online Tool to Study State Health Estimates

Join us for a virtual tour of State Health Compare, a new, user-friendly online tool for obtaining and comparing state-level estimates related to health and health care.

State Health Compare: How's It Different?

State Health Compare combines estimates previously available separately through the SHADAC Data Center and the Robert Wood Johnson Foundation (RWJF) Data Hub. The new, merged tool brings together estimates on a wide range of health-related topics in an effort to allow analysts and policymakers to view state-level data through a broad Culture of Health lens.

The Virtual Tour: What Will You Learn?

The Virtual Tour: What Will You Learn?

Ms. Turner will be joined on the webinar by Carolyn Miller, Senior Program Officer at RWJF, and by SHADAC Director Lynn Blewett. SHADAC Senior Research Fellow Brett Fried will also be available to answer questions.

Blog & News

Lynn Blewett on Health Affairs Blog: How Minnesota Is Stepping Up to Preserve its Individual Market

April 19, 2017:

In a new piece on the Health Affairs Blog, SHADAC Principal Investigator Lynn Blewett explains how Minnesota has emerged as an active state in terms of moving ahead on health care reform. Dr. Blewett's post discusses the state's decision to cap marketplace enrollment as well as the Minnesota legislature's move to pass a premium relief rebate bill.

This piece builds on Dr. Blewett's December blog post about the steps Minnesota is taking to preserve its individual insurance market, particularly in response to the decision of Blue Cross Blue Shield to leave the market.

How Minnesota is Supporting its Individual Market

Dr. Blewett gives an overview of the Health Insurance Premium Relief bill, including the requirements an individual must meet to be eligible for a rebate. Because it is estimated that between 50,000 and 70,000 individuals did not return to the market to purchase coverage, it is expected that Minnesota's uninsured rates will increase by about 20 percent. Reasons for this likely decrease in the number of people purchasing coverage in the state's individual market are attributable to several factors, according to Dr. Blewett. Among these factors are the limited publicity and outreach that followed a highly political rebate agreement, which may have left consumers unaware or confused about the details of the bill. Another factor could have been the apparent increase in employer-sponsored insurance provided by small employers in Minnesota. Dr. Blewett anticipates that the impact of the reduced number of people purchasing coverage through the individual market will be limited, at least in the short term.

The blog also elaborates on Minnesota's Premium Security Plan, which was unable to move out of the state's House or Senate but discussed the source of state funds and contingency language related to Minnesota's 1332 waiver application. An overview of these topics is available in the full post.

Next Steps for Minnesota

A key issue moving forward is the lack of committment by the health plans to reducing premiums and establishing options throughout the state. Dr. Blewett notes that if the plans do not significantly address these concerns, the public option will be "back on the table." MinnesotaCare is a well-liked option, so it might still be a viable option if the private sector is unable to meet the needs of all Minnesotans purchasing coverage in the private market.

Blog & News

NHIS: Coverage and Uninsurance Rates Mostly Stable in January-September 2016

May 17, 2017:The National Center for Health Statistics (NCHS) released health insurance coverage estimates for January through September 20161 from the National Health Interview Survey (NHIS) as part of the NHIS Early Release Program.

In the Nation

With only a few exceptions coverage and uninsurance rates remained stable between the first three quarters of 2015 and the first three quarters of 2016.

Coverage by Type

Adults (18-64 years)

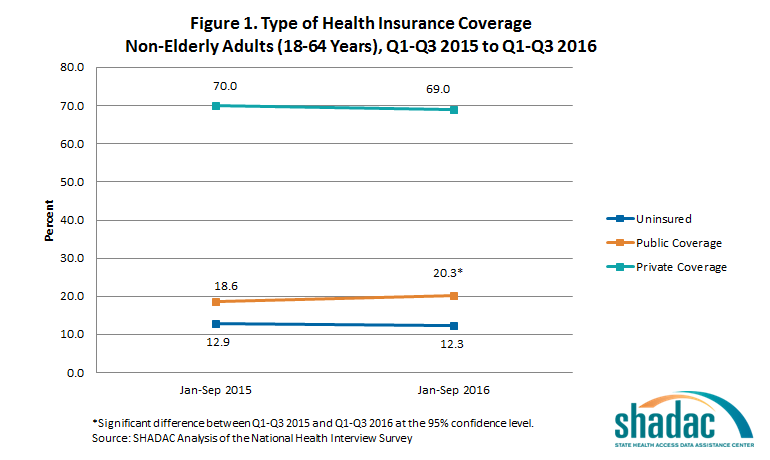

The new estimates show that among adults aged 18 to 64, only the rate of public coverage changed significantly, increasing 1.7 percentage points. Uninsurance and private coverage were statistically stable. Among this group, in the first three quarters of 2016:

- 12.3% were uninsured at the time of interview

- 20.3% had public coverage (vs. 18.6% in January-September 2015)

- 69.0% had private coverage

Children (0-17 years)

The rates of coverage for children (0-17 years) by type of coverage were statistically unchanged from the first three quarters of 2015. Among this group in January through September of 2016:

- 5.0% were uninsured at the time of interview

- 43.4% had public coverage

- 53.5% had private coverage

The Uninsured

Adults (18-64 years)

Not only did uninsurance hold steady from the first three quarters of 2015 and the first three quarters of 2016 among non-elderly adults taken as a whole, but the distribution of uninsurance among subgroups remained stable:

- Adults aged 25 to 34 years continued to be the most likely to be uninsured, with nearly twice the uninsured rate of 45-64 year olds (16.4% vs. 8.6%).

- Adults aged 18 to 24 and adults aged 35 to 44 once again had similar rates of uninsurance, at 13.6 and 14.7, respectively.

Children (0-17 years)

Uninsurace among children was stable overall between January through September 2015 and January through September 2016; however, a breakdown by poverty status and coverage type shows that the percentage of poor children (<100% FPL) with private health insurance coverage decreased significantly, from 9.6 to 7.1 percent.

Race/Ethnicity

The only racial/ethnic group that saw a statistically significant change from January through September 2015 to January through September 2016 was Hispanics/Latinos, among whom uninsurance dropped 2.1 percentage points (from 21% to 18.9%).

Enrollment in High-Deductible Health Plans

Among persons under the age 65 with private health insurance, the percentage who were enrolled in a high deductible health plan (HDHP) increased in 2016. Among this age group:

- 39.1 percent were enrolled in an HDHP (vs. 36.2% in January-September 2015)

- 15.2 percent were enrolled in HDHPs that incorporated health savings accounts (vs. 13.2% in January-September 2015)

In the States

NHIS estimates of the uninsured are available for 38 individual states with sufficient sample size for the first three quarters of the 2016 calendar year. Among states with estimates available for the first three quarters of both 2015 and 2016, the only one that saw a significant change in uninsurance was California, with a decrease of 4.5 percentage points.

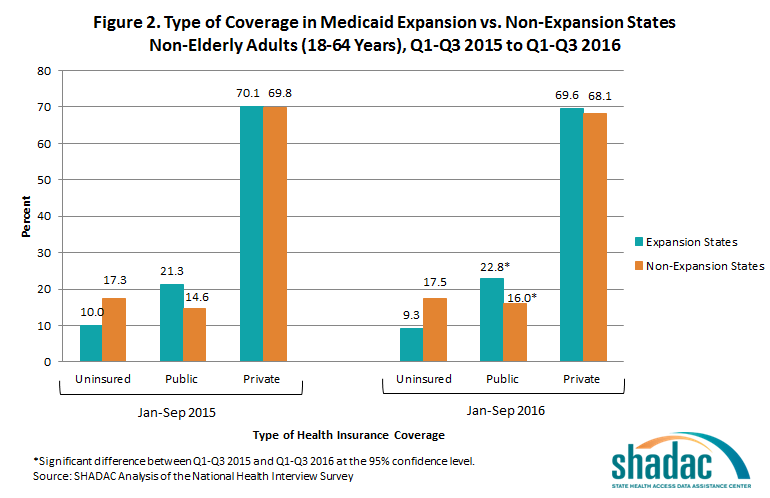

State Medicaid Expansion Status

In both Medicaid expansion states and non-expansion states, rates of public coverage increased significantly among non-elderly adults (18 to 64) from the first three quarters of 2015 to the first three quarters 2016. Uninsurance rates and rates of private coverage held stable in both expansion and non-expansion states.

Among adults ages 18 to 64 living in expansion states:

- 9.3 percent were uninsured at the time of interview

- 69.6 percent had private coverage

- 22.8 percent had public coverage (up from 21.3 % in the first three quarters of 2015)

Among adults ages 18 to 64 living in states that did not expand Medicaid:

- 17.5 percent were uninsured at the time of interview

- 68.1 percent had private coverage

- 16.0 percent had public coverage (up from 14.6% in January through September 2015)

Non-elderly adults in expansion states continued to be less likely to be uninsured than non-elderly adults in non-expansion states in the first three quarters of 2016, with uninsurance in expansion states at 9.3% and uninsurance in non-expansion states at 17.5%.

View the NCHS Early Release Report, "Health Insurance Coverage: Early Release of Esimates from the National Health Interview Survey, January-September 2016."

About the NHIS Early Release Program

The new NHIS estimates were published as part of the NHIS Early Release Program, through which analytic reports and preliminary microdata files are made available on an expedited schedule so that data users have access to the most recent NHIS information without having to wait for the final annual NHIS microdata files to be released after the end of each data collection year. The early release reports and files are produced prior to final data editing and weighting.

1SHADAC's analysis differes slightly from the NCHS report because SHADAC'compares estimates from the first three quarters of 2015 with estimates from the first three quarters of 2016, while the NCHS compares the estimates for all of 2015 with estimates from the first three quarters of 2016.

Blog & News

How Would an ACA Repeal Affect Minnesota?

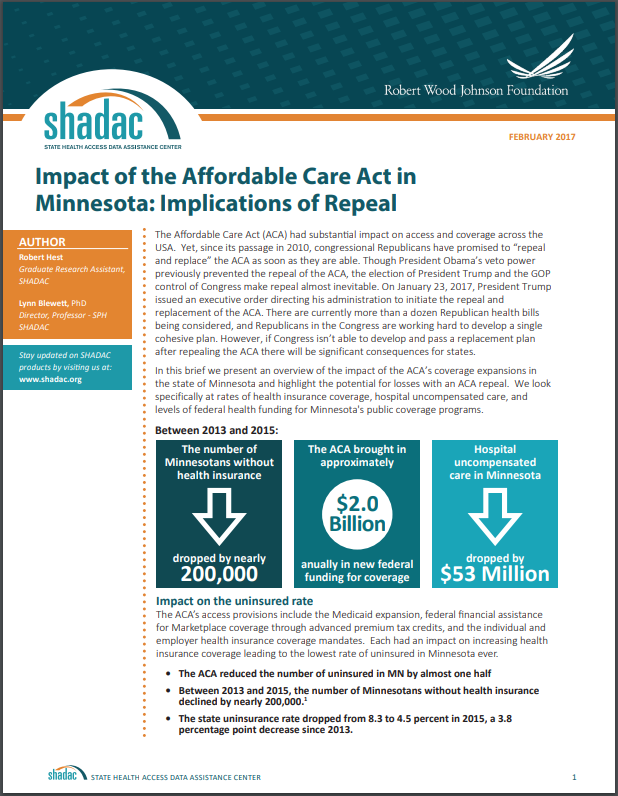

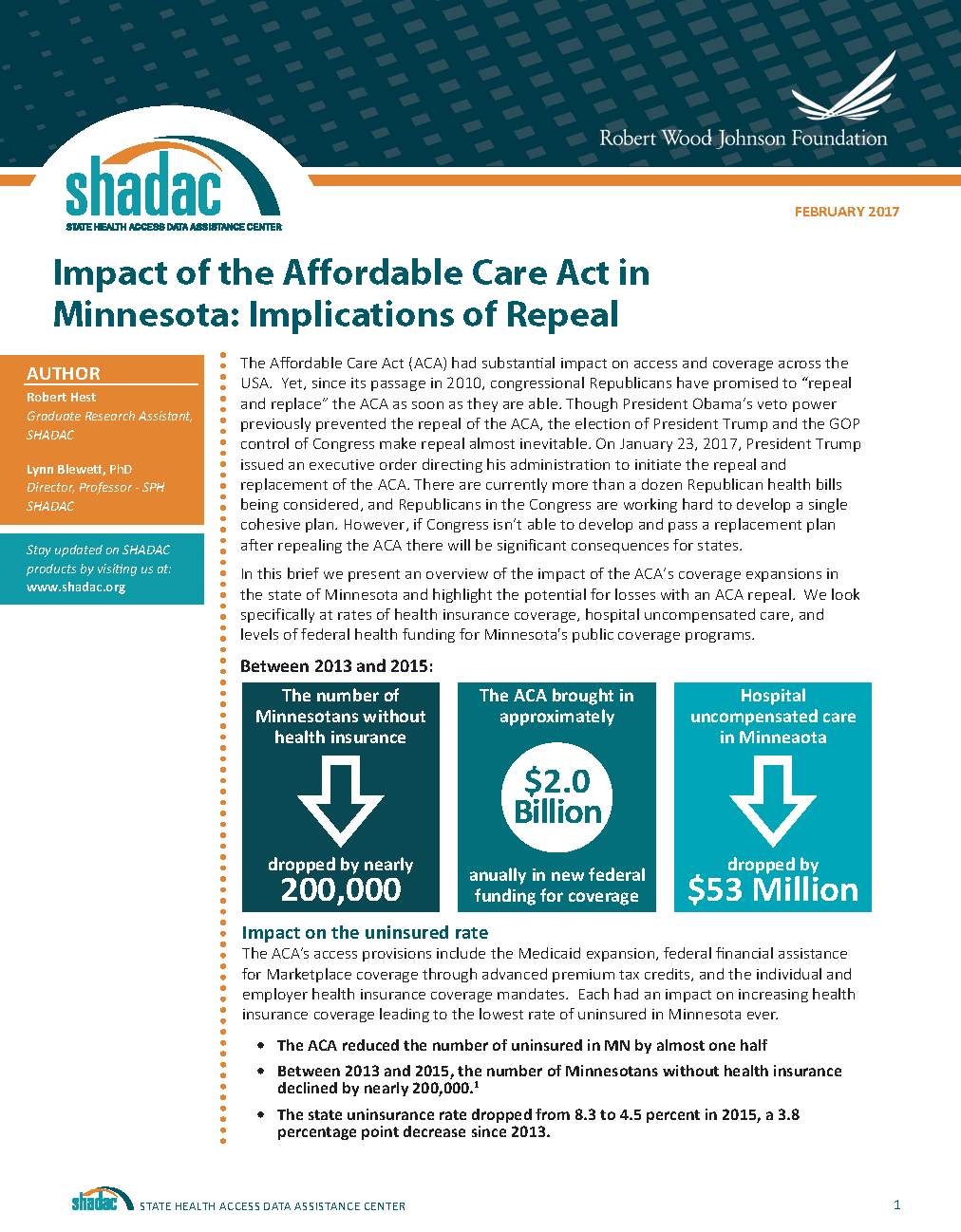

May 11, 2017:A new SHADAC brief examines the implications of an Affordable Care Act repeal for Minnesota. The authors, SHADAC Research Assistant Robert Hest and SHADAC Director Lynn Blewett, present an overview of the the impact of the ACA's coverage expansions in the state and highlight the potential for losses with a repeal. They look specifically at rates of health insurance coverage, hospital uncompensated care, and levels of federal health funding for Minnesota's public coverage programs.

The authors point out that between 2013 and 2015

The authors point out that between 2013 and 2015

- The ACA reduced the number of uninsured in Minnesota by nearly 200,000 (almost one half), bringing the state's uninsurance rate down to 4.5 percent from 8.3 percent. 1

- Minnesota's hospital uncompensated care fell by $53 million (a 16.7 percent decrease). 2

With an ACA repeal

- The number of uninsured Minnesotans would more than double. 3

- Minnesota's hospital uncompensated care would increase by an estimated $548 million by 2019. 4

The authors also emphasize that individuals enrolled in health plans through MNsure received an estimated $115 million in tax credits and cost-sharing reductions from the federal government in 2016--funds that would no longer be available with an ACA repeal. 5 Moreover, the State of Minnesota stands to lose the $2 billion in annual federal funding that it currently receives for Medical Assistance and MinnesotaCare, along with $80.8 million in federal Preventional and Public Health fund grants. 6, 7

1 SHADAC Analysis of the 2013-2015 American Community Survey

2 Minnesota Department of Health: Health Economics Program. "Uncompensated Care at Minnesota Hospitals Drops for the Second Year in a Row," October 31, 2016. http://www.health.state.mn.us/news/pressrel/2016/costs103116.pdf

3 SHADAC Analysis of the 2015 American Community Survey

4 Buettgens, M., Blumber, L., & Holahan, J. "The Impact on Health Care PRoviders of Partial ACA Repeal through Reconciliation," Urban Institute, January 2017. http://www.rwjf.org/content/dam/farm/reports/issue_briefs/2017/rwjf433621

5 Kaiser Family Foundation. "Estimated Total PRemium Tax Credits Received by Marketplace Enrollees," March 31, 2016. http://kff.org/health-reform/state-indicator/average-monthly-advance-premium-tax-credit-aptc/

6 Minnesota Department of Human Services. "Repealing the Affordable Care Act: Impacts to Minnesota's Public Healthcare Programs," January 6, 2017. http://mn.gov/dhs/aca-repeal/issue-brief/

7 Trust for America's Health. "Minnesota Could Lose More than $80 Million to Fight Health Epidemics over Five Years if the ACA and Prevention and Public Health Fund Are Repealed," 2017. http://healthyamericans.org/reports/prevention-fund-state-facts-2017/release.php?stateid=MN

Publication

Impact of the Affordable Care Act in Minnesota: Implications of Repeal

In this brief, the authors present an overview of the impact of the ACA’s coverage expansions in the state of Minnesota and highlight the potential for losses with an ACA repeal. We look specifically at rates of health insurance coverage, hospital uncompensated care, and levels of federal health funding for Minnesota's public coverage programs.