VISIT STATE HEALTH COMPARE

VISIT STATE HEALTH COMPARE

Awarded Grant

How Much Better is Medicaid than Marketplace Coverage at Easing the Burden of Out-of-Pocket Spending for Near-Poor Adults? (December 2016)

Principal Investigator: Frederic Blavin, PhD, The Urban Institute

The goal of this study is to inform expansion and non-expansion states of the effect of Medicaid expansion on out-of-pocket spending and the overall resources available to families. Using data from the 2014-2016 Current Population Survey Annual Social and Economic Supplement, the applicants will conduct a difference-in-differences analysis, using the 2014 Medicaid expansion as a natural experiment, to address the following research questions:

- Compared to marketplace coverage, what is the impact of the Medicaid expansion on reducing premium and non-premium out-of-pocket health spending among low-income adults with incomes between 100 and 138% FPL? In other words, among those in this income group, how much would out-of-pocket health spending in nonexpansion states change if states either expanded Medicaid or made Marketplace benefits and cost-sharing comparable with Medicaid?

- What is the impact of the Medicaid expansion on out-of-pocket health spending among adults with incomes below 100% FPL in expansion states, relative to similar adults in nonexpansion states without access to Medicaid or Marketplace subsidies?

- How do these changes in out-of-pocket spending affect the overall resources available to families?

Publications

Medicaid vs. Marketplace Coverage for Near-Poor Adults: Effects on Out-of-Pocket Spending and Coverage

(June 2018, Presentation)

"Medicaid Versus Marketplace Coverage for Near-Poor Adults: Effects On Out-Of-Pocket Spending"

(February 2018, Health Affairs)

Impact of Medicaid vs. Marketplace Coverage on Out-of-Pocket Spending for Near-Poor Adults

(December 2017, SHARE Webinar)

Medicaid vs. Marketplace Coverage for Near-Poor Adults: Impact on Out-of-Pocket Spending Burdens

(November 2017, Presentation)

Blog & News

Video: Angie Fertig Discusses SHARE-Funded Study of Pent-Up Demand among New Medicaid Enrollees

November 11, 2016:Dr. Angie Fertig, Research Investigator at Medica Research Institute (MRI), is featured in a new MRI Investigator Video in which she discusses her SHARE-funded analysis of pent-up demand among new Medicaid enrollees under the ACA. Check out the video below.

Additional information about this analysis can be found on Dr. Fertig's SHARE grantee page.

Angela Fertig PhD-2016 from Medica Research Institute on Vimeo.

Blog & News

More Employees Chose High-Deductible Plans in 2015

December 22, 2016:With the recent focus on health insurance coverage purchased through Affordable Care Act marketplaces, it is easy to forget that the majority of individuals are enrolled in health insurance through their employer (56% in 2015).[1] This blog is the first in a series that highlights the experiences of individuals enrolled in private sector employer-sponsored insurance. It uses data from the Medical Expenditure Panel Survey-Insurance Component (MEPS-IC) recently collected by the Agency for Healthcare Research and Quality (AHRQ).

What is a high-deductible health plan?

A plan with a deductible requires an upfront payment for medical services before insurance coverage kicks in. For example, if the deductible is set at $500, the individual must pay all of the expenses of any covered medical treatment up to $500. After the deductible has “been met” (i.e., the individual has paid for $500 worth of medical bills), all medical bills greater than the $500 deductible are covered by the health plan.

For the purposes of our analysis, high-deductible plans are defined as plans that meet the minimum deductible amount required for Health Savings Account (HSA) eligibility — $1,300 for an individual and $2,600 for a family in 2015).

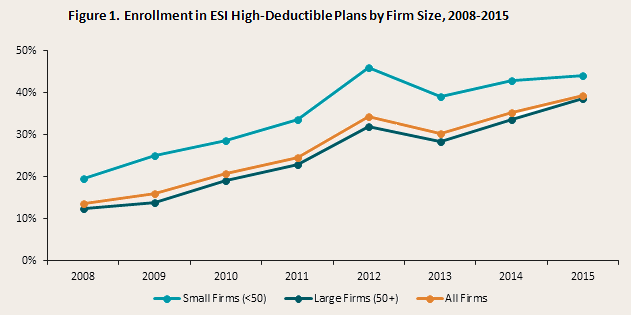

Enrollment in high-deductible plans has been increasing steadily.

In 2015, almost 40% of private sector workers were enrolled in a high-deductible plan through their employer (Figure 1). This represents an almost threefold increase between 2008 and 2015. While the growth trend among these plans is similar for large and small firms, workers in small firms have had historically higher enrollment in high-deductible plans.

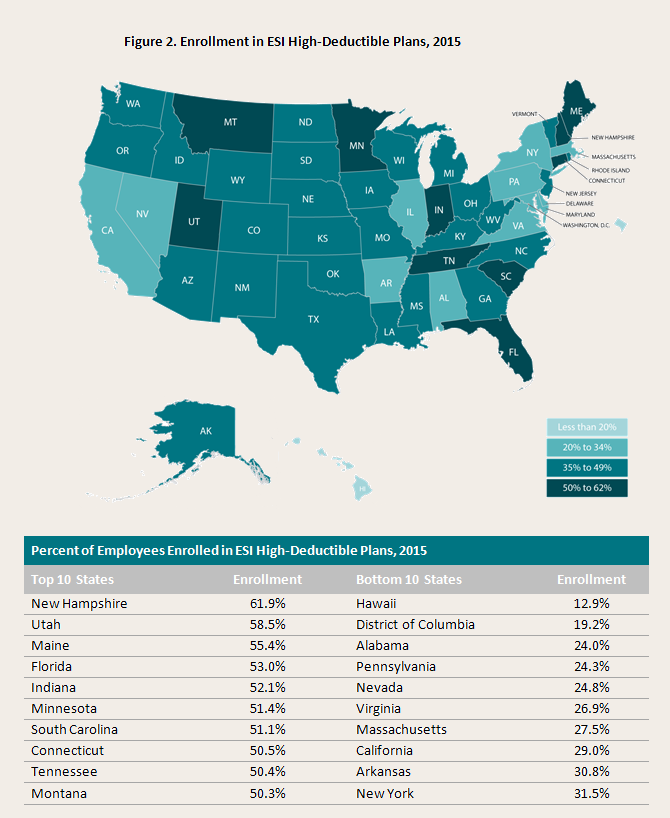

Enrollment in high-deductible plans varies across the country.

The percent of workers enrolled in employer-sponsored plans with high deductibles varied widely by state in 2015, from 12.9% in Hawaii to 61.9% in New Hampshire. Among firms of all sizes, enrollment in high-deductible plans was at least 50% in ten states and below 30% in just eight states and the District of Columbia in 2015.

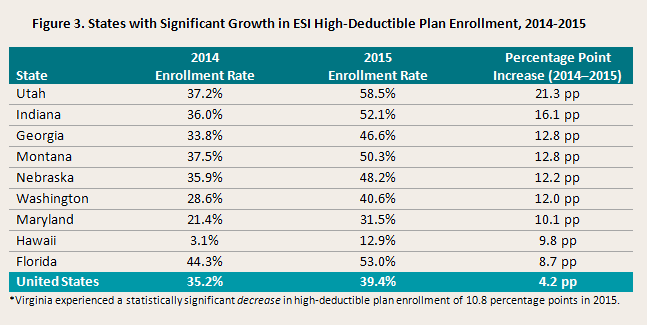

Nine states saw significant increases in high-deductible enrollment.

National growth in high-deductible plans between 2014 and 2015 seems to have been driven by a relatively small number of states. While roughly three quarters of the states experienced some increase in the percent of private-sector employees enrolled in high-deductible plans, only nine states saw a statistically significant increase (this represents fewer states with statistically significant increases compared to 2013–2014).

Why are more people enrolling in high-deductible plans?

High-deductible plans have become increasingly popular over recent years because they help to keep premiums affordable, thereby helping get more people covered, and they are meant to provide an incentive for people to (a) use medical care only when they need it and (b) shop around for the care they do use.

The advantage of high-deductible plans is that they tend to have lower premiums — making health insurance more affordable and accessible. Additionally, deductibles do not apply to preventive services — including screenings, immunizations, and an annual physical — which must be provided with no out-of-pocket payment under the Affordable Care Act.

The main disadvantage of high-deductible plans is that the higher deductibles may act as a significant barrier to getting needed care. This can be especially problematic for people with chronic conditions or those facing a medical emergency. Also, while deductibles do not apply to preventive services as defined by the Affordable Care Act, there may be confusion about this among high-deductible plan enrollees who may unnecessarily forgo preventive care due to cost concerns. In addition, it can be difficult to understand what payments are eligible to contribute toward one's deductible. In most cases, payments for services provided by out-of-network providers or for non-covered benefits (e.g., vision, dental, over-the-counter medicines, brand name prescriptions, etc.) do not count toward the deductible. Finally, hospitals and other providers have raised concerns about the difficulty of collecting the required out-of-pocket payments at the point of service, a challenge that can contribute to bad medical debt.

Notes: This analysis focuses on private sector workers. Small firms are defined as having fewer than 50 employees, and large firms are defined as having 50 or more employees. High-Deductible Plans are defined as plans that meet the minimum deductible amount required for Health Savings Account (HSA) eligibility (i.e., $1,300 for an individual and $2,600 for a family in 2015). Findings are based on SHADAC analysis of the Medical Expenditure Panel Survey - Insurance Component. Changes are statistically significant at the 95 percent confidence level.

[1] Barnett, J.C., & Vornovitsky, M. September 13, 2016. “Health Insurance Coverage in the United States: 2015.” Current Population Reports. Washington, DC: U.S. Census Bureau. Available at http://www.census.gov/content/dam/Census/library/publications/2016/demo/p60-257.pdf

Blog & News

SHARE Research at APPAM: A State Perspective on the Coverage, Access, & Cost Impacts of the ACA

November 02, 2016:The 2016 Fall Research Conference of the Association for Public Policy Analysis & Management (APPAM) begins tomorrow and runs through Friday in Washington, DC. The conference, which is mutli-displinary in nature, focuses on a range of current and emerging policy and management issues, including health policy. This year's conference theme is "The Role of Research in Making Government More Effective."

Findings from several SHARE-funded studies will be featured during the conference on a panel titled, "State-Level Impacts of the Affordable Care Act: Coverage, Access, and Costs." The panel includes four presentations that examine the effects of the federal Affordable Care Act (ACA) on a range of outcomes, including health insurance coverage, access to care, service utilization, and costs and affordability. In each study, the researchers examine outcomes as a function of state health policy decisions and attributes.

SHARE funded three of these four studies and organized this panel with a state policy lens in mind – recognizing that the impacts of the ACA hinge on individual state decisions and that the ACA, because of its federal scope, provides a unique opportunity to study state variation in a systematic way. The systematic nature of these analyses subsequently supports the generation of evidence that can meaningfully inform and facilitate federal and state policymaking and public management in the areas of health insurance coverage and insurance market regulation.

Click on the links below to learn more about the panel and/or the individual panel presentations.

Panel Details

State-Level Impacts of the Affordable Care Act: Coverage, Access, and Costs

Thursday, November 3, 2016, 1:15PM – 2:45PM

Room: Columbia 9 (Washington Hilton)

Chair: Sharon Long, Urban Institute

Discussants: Kathleen Call, State Health Access Data Assistance Center, and Lisa Dubay, Urban Institute

To Expand Medicaid or Not to Expand Medicaid? Effects of State ACA Medicaid Expansion Decisions on Coverage, Access, Utilization, and Health Status of Low-Income Adults

Speaker: Laura Wherry, University of California, Los Angeles

The Medicaid Expansion States: Effects of Medicaid Coverage on Access, Affordability, Utilization, and Health Status for Newly Eligible and Previously Eligible Adults*

Speaker: Michael Dworsky, RAND Corporation

Early Evidence on Employment Responses to the Affordable Care Act: Employer Coverage Offers*

Speaker: Jean Abraham, University of Minnesota

Specialty Drug Benefit Design and Patient Out-of-Pocket Costs in the ACA Health Insurance Exchanges*

Speaker: Erin Taylor, Pardee RAND Graduate School

*Research supported by SHARE funding

Publication

Comparing Federal Government Surveys That Count the Uninsured: 2016

This brief provides an annual update to comparisons of uninsurance estimates from four federal surveys1:

- The American Community Survey (ACS)

- The Current Population Survey (CPS)

- The Medical Expenditure Panel Survey - Household Component (MEPS-HC)

- The National Health Interview Survey (NHIS)

In this brief, we present current and historical national estimates of uininsurance along with the most recent avaialble state-level estimates from these surveys. We also discuss the main reasons for variation in the estimates across the different surveys.

1Another federal survey that provides estimates of the uninsured is the Behavioral Risk Factor Surveillance System (BRFSS), which provides uninsurance estimates for non-elderly adults (ages 18 to 64) nationally and among states. Details about the BRFSS are included in Appendix A of the brief, and estimates from the BRFSS are provided in Appendix B.