| ESI PRODUCTS |

|

State Profiles 50-State Comparison Tables

Interactive Maps See the bottom of the companion blog for an interactive map showing levels of, and changes in, average annual premiums for single and family coverage in 2019. |

Introduction

The arrival of the novel coronavirus has not only disrupted many patterns of life and work in the United States and internationally, but exacerbated many long-standing concerns regarding health care affordability, access, and utilization as well as rates of health insurance coverage for Americans. For instance, in April 2020 SHADAC fielded an AmeriSpeak Omnibus survey, conducted by NORC, which found that due to the pandemic, over 7 million U.S. adults delayed needed care and over 10 million adults lost their health insurance coverage.1

Despite record spikes in unemployment and corresponding health insurance coverage losses attributed to the pandemic (estimated in the tens of millions), employer-sponsored health insurance (ESI) remains the largest source of coverage for Americans,2 with 62.5 million private-sector employees enrolled in ESI in 2019.

Though data for 2020 will not be available until 2021, it is still important to monitor and understand long-running trends in affordability and access in this critical market. Understanding 2019 coverage data will also provide an important baseline for measuring the ongoing fluctuations in the number of workers covered by ESI until the pandemic eases.

To this end, SHADAC presents four related products analyzing the experiences of private-sector employees who had ESI over the period of 2015-2019: a series of individual state profiles highlighting ESI trends, a national-level infographic with an accompanying blog, 50-state data tables, and a 50-state interactive map showing levels of, and changes in, average annual premiums for single coverage in 2019. These analyses use estimates from the Medical Expenditure Panel Survey–Insurance Component (MEPS–IC), recently produced by the Agency for Healthcare Research and Quality (AHRQ).

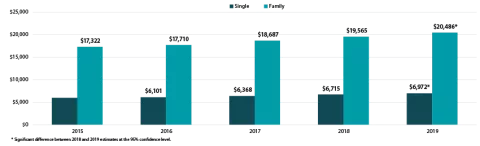

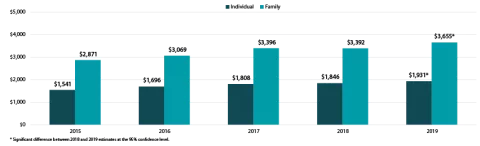

This brief narrative provides an overview of the trends in affordability of ESI coverage and employees’ access to ESI. As in previous years, ESI premiums are high and have continued to increase—the average premium for family coverage was nearly $20,500 per year in 2019. In addition, employees with ESI face substantial cost sharing, with average annual deductibles of more than $1,931 for single coverage and $3,655 for family coverage in 2019. Additionally, more than half (50.5 percent) of employees receiving ESI nationwide were enrolled in a high-deductible health plan (HDHP).3

Premiums rose nationally and in 13 states in 2019

Among private sector workers who receive ESI, average annual premiums increased nationally and in 13 states (including D.C.) between 2018 and 2019. No states experienced decreases in average premiums over that period. Nationally, single premiums increased 3.8 percent ($257) from $6,715 in 2018 to $6,972 in 2019. Family premiums increased 4.7 percent ($921) from $19,565 in 2018 to $20,486 in 2019. This follows a near decades-long trend of premium increases—between 2002 and 2019, single premiums increased 119 percent ($3,783) and family premiums increased 142 percent ($12,017).4

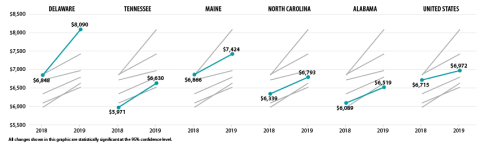

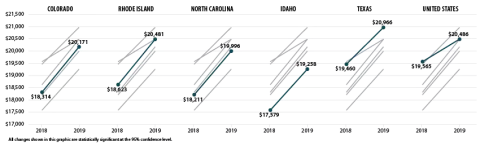

Delaware saw the largest percentage increase in single premiums at 18.1 percent (or $1,242) from $6,848 in 2018 to $8,090 in 2019, and Colorado had the largest increase in family premiums at 10.1 percent (or $1,857) from $18,314 in 2018 to $20,171 in 2019. The chart below shows trends in single and family premiums for the states with the largest significant increases in single or family premiums between 2018 and 2019.

Average Single and Family Premiums, 2015-2019

States with the Largest Increases in Average Single Premiums, 2018-2019

States with the Largest Increases in Average Family Premiums, 2018-2019

Premiums also ranged significantly across the states in 2019, from $6,054 in Arkansas to $8,933 in Alaska for single coverage and from $17,734 in Alabama to $22,969 in Alaska for family coverage.

Deductibles rose nationally and in 10 states

Employees with coverage through their employer continued to face large and rising deductibles in 2019. Nationally, the average deductible reached $1,931 (an increase from $1,846 in 2018) for individuals and $3,655 for families (an increase from $3,392 in 2018). Eight states saw increases in individual deductibles, and seven states saw increases in family deductibles.

Only Pennsylvania saw a decline in average individual deductibles, falling by $73, from $1,831 in 2018 to $1,646 in 2019.

Average Individual and Family Deductibles, 2015-2019

There was a great deal of variation across states in the size of deductibles, ranging from $1,267 in Hawaii to $2,521 in Montana for individual deductibles and from $2,619 in Hawaii to $4,615 in Tennessee for family deductibles.

High-deductible health plan enrollment changes across the states

Nationwide, the percent of employees enrolled in a high-deductible health plan (HDHP) held steady in 2019 at 50.5 percent. This was the second consecutive year of no significant national change in HDHP enrollment.

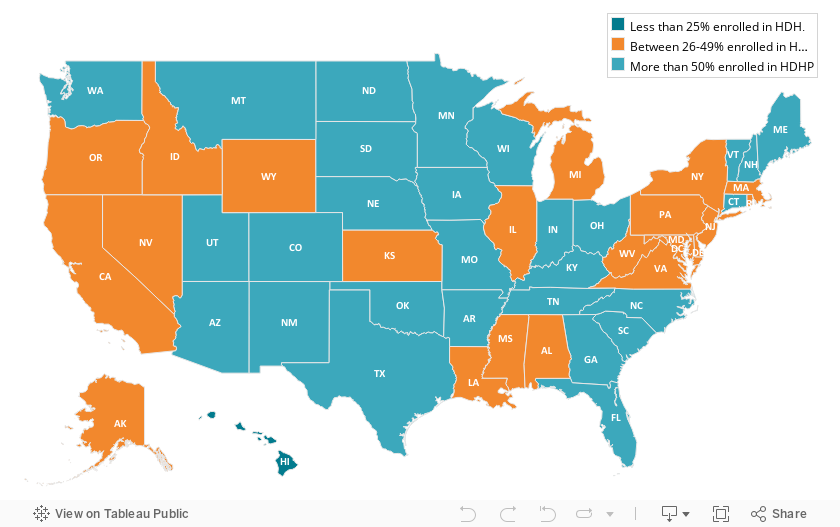

Percent of employees enrolled in a high-deductible health plan by state, 2019

Interactive Map: Hover over a state on the map below to view the percent of employees enrolled in a HDHP in 2019, or click a state to view and download its individual state profile.

Examining HDHP enrollment at the state level reveals some interesting changes between last year and the year prior. In 2018, a majority of employees were enrolled in a HDHP in nine states. In 2019, however, a majority of employees were enrolled in a HDHP in 28 states, as illustrated by the above map. Additionally, in just one state (Hawaii) less than a quarter of employees were enrolled in an HDHP.

Employees’ access to employer-sponsored coverage largely unchanged in 2019

Employee access to ESI has three components:

1. Employee Offer: An employee must work in an establishment that offers coverage.

2. Employee Eligibility: An employee must meet the criteria established by the employer to be eligible for coverage that is offered. (For example, the employee might have to work a minimum number of hours per pay period or complete a minimum length of service with the employer in order to be eligible.)

3. Employee Take-Up: The employee must decide to enroll in (“take up”) the offer of ESI coverage.

Less than half (47.4 percent) of private-sector establishments offered coverage to their employees in 2019, statistically unchanged from 2018. Substantial variation across the states remained, with offer rates ranging from 37.9 percent in Utah to 84.1 percent in Hawaii.5

Nationally, 85.3 percent of employees worked at an establishment that offered ESI in 2019, a slight increase from 2018. This was driven by an increase in three states (Delaware, New Jersey, and South Carolina); no states saw a decrease in the percent of employees in establishments that offer coverage.

Among employees working at an offering establishment, 77.7 percent were eligible for ESI coverage in 2019 (no change from 2018). In 2018, three states (Kansas, New Mexico, and South Dakota) saw increases in the eligibility rate; no states saw a decrease.

Among employees eligible for coverage, 71.9 percent enrolled in ESI in 2019 (statistically unchanged from 2018), and only two states (Connecticut and Utah) saw a decline in enrollment.

It is important to remember that these trends pre-date the COVID-19 pandemic and the associated employment losses. It is likely that millions of Americans have lost ESI coverage since March of 2020. It seems likely, however, that the long-running trends in health care costs remain unchanged—our analysis shows continued increase in premiums and deductibles and high rates of enrollment in HDHP.

For more detailed information on ESI findings from SHADAC, see the following products:

- Printable version of this ESI Report Narrative

- Companion Blog and Infographic highlighting key findings at the national level regarding ESI coverage affordability and access

- Two-page profiles on ESI trends for each state

- 50-state interactive map showing levels of, and changes in, average annual premiums for single and family coverage in 2019, with links to state profile pages

- 50-state comparison tables including 2015-2019 ESI data

Notes and Sources

Notes. All changes and differences described in this report are statistically significant at the 95 percent confidence level, unless otherwise specified. This analysis and linked products only pertain to employers, establishments, and employees in the private sector. Average premium prices have not been adjusted to account for variation in actuarial value.

Sources. Data are from the 2015–2019 Medical Expenditure Panel Survey–Insurance Component (MEPS-IC), produced by the Agency for Healthcare Research and Quality (AHRQ) and are available on SHADAC’s State Health Compare web tool at statehealthcompare.shadac.org.

References

1 State Health Access Data Assistance Center (SHADAC). (2020, August 24). SHADAC COVID-19 Survey Chartbooks Provide Visualizations of Coronavirus Impacts of Health Insurance Coverage, Access and Affordability of Care, and Pandemic Stress Levels of U.S. Adults. Available at https://shadac.org/SHADAC-COVID-19-Survey-Chartbooks

2 Zipperer, B. & Bivens, J. (2020, May 14). 16.2 million workers have likely lost employer-provided health insurance since the coronavirus shock began. Retrieved from https://www.epi.org/blog/16-2-million-workers-have-likely-lost-employer-provided-health-insurance-since-the-coronavirus-shock-began/

Golberstein, E., Abraham, J.M., Blewett, L.A., Fried, B., Hest, R., & Lukanen, E. (April 2020). University of Minnesota COVID-19 Health Insurance Model estimates that as many as 18.4 million individuals may be at risk of losing their employer-sponsored health insurance coverage (ESI). Available at https://shadac.org/publications/COVID-19-MNHealth-Insurance-Model

Health Management Associates (HMA). (2020, April 3). COVID-19 Impact on Medicaid, Marketplace, and the Uninsured, by State. Retrieved from https://www.healthmanagement.com/wp-content/uploads/HMA-Estimates-of-COVID-Impact-on-Coverage-public-version-for-April-3-830-CT.pdf

3 Defined as plans that qualify for a tax-advantaged health savings account. In 2019, qualifying plans had to have an annual deductible of at least $1,350 for individual coverage or at least $2,700 for family coverage.

4 State Health Compare. (2020). Average Annual ESI Premium: 2002-2019 [data set]. Available at http://statehealthcompare.shadac.org/trend/34/average-annual-employer-sponsored-insurance-premium-by-plan-type#14/1/57,58/9,10,11,12,13,1,2,3,4,5,6,7,8,15,24,25,27/65

5 Hawaii has a broad employer mandate that preceded the ACA. The Hawaii Prepaid Health Care Act, enacted in 1974, requires private employers to provide health insurance for employees who work at least 20 hours (some exceptions apply).