VISIT STATE HEALTH COMPARE

VISIT STATE HEALTH COMPARE

Blog & News

Alternatives to ACA Compliant Plans in the Individual Market

November 15, 2019: Introduction

Introduction

Change is constant in the nongroup health insurance market, and both recent and forthcoming regulation changes might pose a threat to market stability. So far, these regulation changes include eliminating the individual mandate tax penalty; eliminating cost sharing payments in 2017; reducing funding for ACA navigator services; and invalidating the guarantee issue and community rating provisions of the ACA.[1]

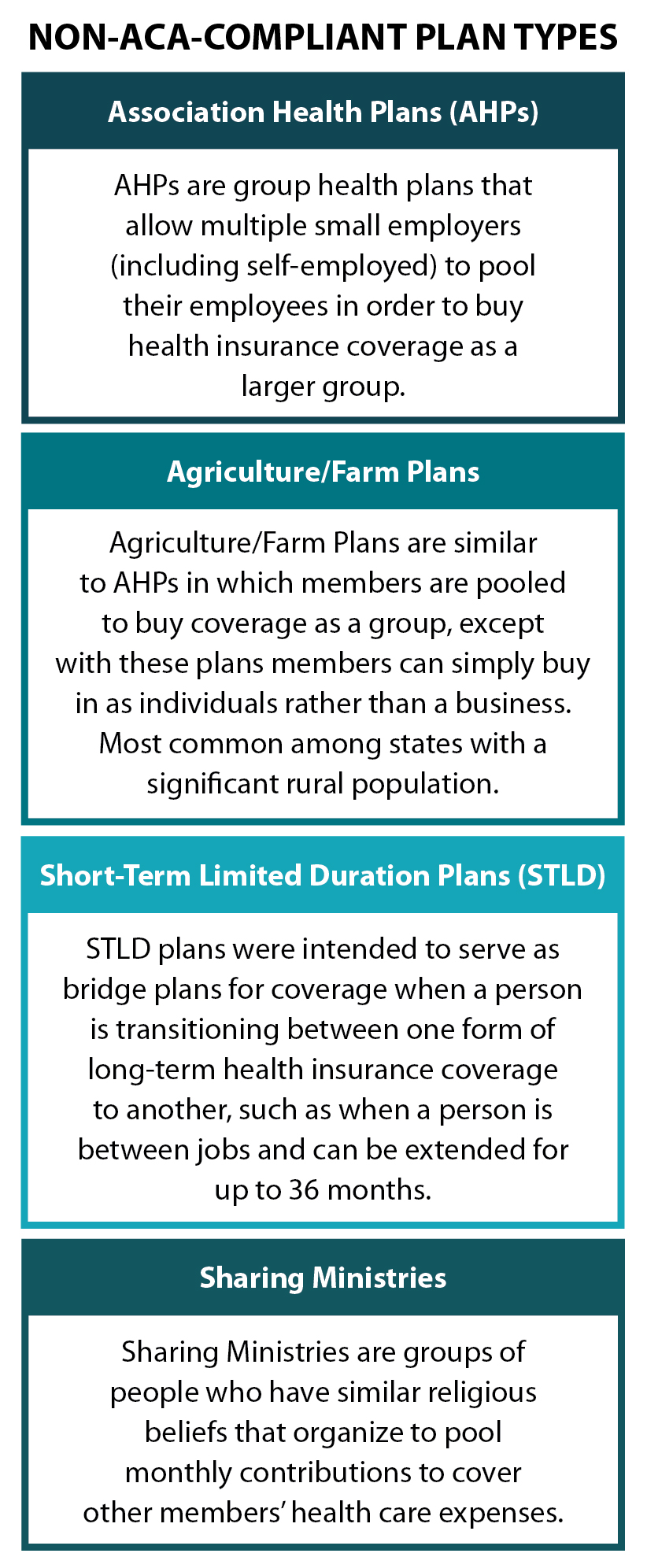

Non-ACA-compliant health plans, which the Academy of Actuaries includes on its list of “major drivers of 2019 premium changes,” may be the greatest factor affecting market stability, however.[2] These plans include Association Health Plans (AHPs), Short-Term Limited Duration plans (STLD), Agriculture/Farm Plans, and religiously based, pre-paid coverage plans, or “Sharing Ministries.” The alternative plans are cheaper than existing products, but they are not required to cover pre-existing health conditions, to maintain minimum medical loss ratios, to cover essential health benefits, or to not discriminate in rating based on gender and health status. With the individual mandate tax penalty no longer enforced, enrollment in non-compliant plans may soon be growing more rapidly.

We investigated each of the non-ACA-compliant plan types and provide a brief description along with current estimates of enrollment or projected enrollment.

Association Health Plans

Association Health Plans (AHP) allow multiple small employers (including self-employed) to pool their employees in order to buy health insurance coverage as a larger group. In June 2018, the Labor Department finalized new rules that widen access to AHPs by greatly loosening previous requirements that ensured these groups had “bona fide” association status. The new rules allow sole proprietors and/or small businesses to band together explicitly to purchase insurance, raising concerns for both the individual and the small-group markets, which have the same set of consumer protections as the ACA-regulated individual market.

Some ACA regulations still apply to AHPs, as they are considered large-group coverage.[3] AHPs must comply with out-of-pocket maximums and cannot impose lifetime limits on coverage. However, while AHPs cannot discriminate against those with pre-existing conditions, they can set premiums based on type of employment, gender, age, and geographic location. They also are not required to cover the ten essential health benefits included in the ACA, with the exception that employers with fifteen employees or more must offer maternity benefits.[4]

Avalere estimates that 3.2 million people will move from ACA compliant plans into AHPs by 2022—1 million from the individual market and the rest from the small group market. They also estimate a resultant premium increase of 3.5 percent for those remaining in the ACA-compliant individual market, which may cause an estimated 130,000 individuals to become newly uninsured.[5]

Agriculture/Farm Bureau Plans

Several states with a significant rural population have looked for regulatory relief through a type of coverage initially targeted to famers and farm-related businesses. These Farm Bureau Plans are similar to AHPs except that members do not need to be businesses; they can simply be individuals. In some states, members do not even need to be farmers or connected with agriculture to join the association. The leading state farm bureau plans include the Farm Bureau Health Plans in Tennessee, Minnesota’s Agriculture Co-ops, and Iowa’s agriculture health plans.

Farm Bureau Health Plans (Tennessee)

Despite implementation of the ACA, Tennessee has continuously allowed its Farm Bureau to sell non-ACA-compliant plans to individuals outside of the ACA’s marketplace. These plans do not have to comply with basic ACA requirements including the mandate to provide essential health benefits and to offer coverage to individuals with pre-existing conditions. In fact, these plans are underwritten and sold just as they were pre-ACA. In the first few years post-ACA, implementation enrollees were supposed to pay the tax penalty for not enrolling in a compliant plan; however, that penalty no longer exists as a deterrent in 2019.

Tennessee’s Farm Bureau Health Plans are regulated by the state as a “not-for-profit membership organization” and are explicitly considered “not insurance.” This status exempts the Farm Bureau Health Plan from all state insurance laws and the insurance regulations adopted under the ACA.[6] The Farm Bureau Plans are underwritten and include a six- to twelve-month pre-existing condition coverage waiting period and a nine-month maternity-coverage waiting period for 2+ person families. Maternity benefits are not available in single coverage plans.

Anyone can join the Farm Bureau for a fee of just $25 a year. Farm Bureau enrollment saw rapid growth in the years since the ACA’s enactment. An estimated 73,000 individuals are enrolled in Tennessee’s Farm Bureau Plan[7] compared to the approximately 209,499 Tennesseans who purchased coverage on the health insurance exchange in 2018, 90 percent of whom received federal subsidies.[8] Tennessee has also had among the highest ACA non-group market premiums in the country.[9]

Minnesota Agriculture Cooperatives

Minnesota passed legislation in 2017 that allowed for the formation of agricultural cooperatives to operate self-funded health plans. Unlike in Tennessee, plan membership is restricted to farmers or people in the agriculture industry, ensuring they can form a true cooperative and self-insure to provide health insurance coverage to members. The farm co-op’s plans accept all who apply but are underwritten such that people with prior health conditions can be charged higher premiums.[10]

In 2018, an estimated 1,700 Minnesotans enrolled in two agricultural cooperative health plans—40 Square Cooperative Solutions and Land O’Lakes Minnesota Co-op Health Plan.[11] This was just one percent of the estimated 166,000 individuals purchasing coverage in the state’s non-group market.

Iowa Association Health Plans

Iowa passed legislation in 2018 to allow for agriculture health co-ops, but following Tennessee’s model rather than Minnesota’s. The Iowa Farm Bureau partnered with Wellmark (Blue Cross) on a new self-funded benefit plan. The state’s legislation requires that the health plan be sponsored by a local nonprofit agriculture organization and explicitly defines the plan as “not insurance,” exempting the plan from most state insurance regulation as well as regulation required under the ACA. As in Tennessee, the Iowa Farm Bureau is not restricted to the agricultural community.[12]

Iowa’s Farm Bureau products were first offered in the fall of 2018 for coverage that began in January 2019. Iowa Farm Bureau offers three health plan options, including two traditional copay or coinsurance plans and one high deductible plan with an HAS. All beneficiaries are subject to underwriting to determine the price of their plan. The Bureau estimated that about half of its current 150,000 families would sign up. They estimated that another 60,000 families may opt to join the Bureau for an annual fee of $55 in order to access its health plan.[13] If these estimates are accurate, the Farm Bureau will have enrolled more than twice the number of individuals that purchased coverage on Iowa’s health insurance exchange in 2018.[14]

Short-Term Limited Duration Plans

In February 2018, the Department of Health and Human Services proposed to broaden Americans’ ability to rely on short-term health plans that, like AHPs, circumvent the ACA’s required benefits and other protections. Short-term Limited Duration (STLD) plans were intended to serve as bridge plans for coverage when a person is transitioning between one form of long-term health insurance coverage to another, such as when a person is between jobs. In an attempt to create more affordable options in the individual market, the Administration proposed rules to allow these plans to extend coverage from the current three-month limit to up to one year, with renewal options.[15] Final rules were issued on August 1, 2018, and plans were offered in October for 2019 coverage. Despite efforts to overturn the rule through the first half of 2019, it was ultimately upheld by a federal district court judge.[16] The final rule allows for extensions of up to 36 months and includes a requirement notice that alerts consumers to the fact that the coverage does not meet the “minimum essential coverage” requirements of the ACA.

Demand for short-term plans has steadily increased since the ACA’s implementation; short-term applications accounted for 57 percent of all combined short-term and major medical plan applications received by eHealth in 2017, up from 47 percent in 2016.[17] According to the National Association of Insurance Commissioners (NAIC), there were at least 160,000 people covered by short-term policies at the end of December 2016, although the total likely exceeds that as there are no consistent reporting requirements for these types of bridge plans.

Typically, because of underwriting and the ability to exclude coverage for those with pre-existing conditions and impose lifetime limits, enrollees in STLD plans tend to be younger and healthier. Estimates vary for the projected enrollment impact of STLD plan expansion. The CMS actuary estimated that 1.7 million people would enroll in short-term plans by 2022,[18] but the Urban Institute projects 4.2 million, 9 and RAND estimates five million people would enroll.[19] Importantly, many of these projected enrollees are people who are currently uninsured—as many as 500,000 based on CMS regulatory analysis.[20]

Sharing Ministries

Sharing ministries are groups of people who have similar faith beliefs that organize to pool resources to cover members’ health care expenses. The ACA and many state statutes explicitly note that sharing ministries are “not insurance” and therefore are exempt from state and federal insurance regulations.

The sharing ministries model is similar to that of the “three-share” safety net programs, or Local Access to Care Programs (LACPs),[21] of the early 90s, wherein enrollees contribute a monthly fee to cover members’ health care costs. Because there is no transfer of risk through an insurance premium, this model is not considered traditional insurance. Typically, sharing ministry plans are locally run and may use a third party to negotiate discounted payment rates with a network of local providers. Other organizations rely on individuals to negotiate their own discounts and payment rates before they seek reimbursement from the plan.

Twenty-one states have laws saying health care sharing ministries are “not insurance.”[22] According to the Alliance of Health Care Sharing Ministries, there are 104 sharing ministries with over 960,000 members.[23] An estimated 90 percent of the ministries are Mennonite/Old German Baptist Christian associations with closed membership. Many require a signature or faith leader attestation of the member’s regular church attendance or commitment to certain religious beliefs and values.[24]

Future Enrollment Projections and Uncertainty

There are many unknowns that make projecting the impact of the non-ACA-compliant plans difficult. Health plans will make their decisions to move into this market based in part on the state regulation, restriction, or even taxation of non-compliant offerings. Based on these uncertainties, the projections of enrollment in Short-Term Limited Duration plans vary greatly, ranging from 1.7 million to 5 million projected enrollees over time, with a small proportion (500,000 based on CMS projections) being newly insured.

The projections for enrollment in Association Health Plans are also varied—Avalere estimates that 3.2 million people will move from compliant to non-compliant plans by 2022 and 130,000 individuals will be newly uninsured. In many ways the true outcome depends on additional changes made at the federal level and regulatory actions taken at the state level.

The tax penalty associated with the individual mandate has, in the past, been a deterrent to buying non-compliant plans. But now that the penalty has been repealed, states could see greater marketing and uptake of non-compliant plans.

Sources

[1] Sanger-Katz, M. (2018, June 12). The new Obamacare lawsuit could undo far more than protections for pre-existing conditions. The New York Times (The Upshot). Retrieved from http://www.nytimes.com/ 2018/06/12/upshot/the-new-obamacare-lawsuit-could-undo-far-more-than-protections-for-pre-existing-conditions.html

[2] American Academy of Actuaries. (2018). Drivers of 2019 Health Insurance Premium Changes. Issue Brief: June 2018. Retrieved from http://www.actuary.org/content/drivers-2019-health-insurance-premium-changes-1

[3] Corlette, S., Hammerquist, J., & Nakahata, P. (2018). New rules to expand association health plans [web exclusive]. The Actuary Magazine. Retrieved from https://theactuarymagazine.org/new-rules-to-expand-association-health-plans/

[4] Andrews, M. (2018). Read the fine print before picking an association plan for your small business. National Public Radio, Kaiser Health News. Retrieved from https://www.npr.org/ sections/health-shots/2018/06/27/623626154/read-the-fine-print-before-picking-bout-an-association-plan-for-your-small-busin

[5] Mendelson, D., Sloan, C., & Brooker, C. (2018). Association health plans projected to enroll 3.2m individuals. Retrieved from http://avalere.com/expertise/managed-care/insights/association-health-plans-projected-to-enroll-3.2m-individuals

[6] Henry J. Kaiser Family Foundation. (2018). Marketplace enrollment, 2014-2018. Retrieved from https://www.kff.org/health-reform/state-indicator/marketplace-enrollment-2014-2017/?currentTimeframe=0&sortModel=%7B%22colId%22:%22Location%22,%22sort%22:%22asc%22%7D

[7] Managed Care. (2017). Tennessee: individual market just barely viable–for now. Retrieved from https://www.managedcaremag.com/archives/2017/7/tennessee-individual-market-just-barely-viable-now

[8] Blumberg, L.J., Buettgens, M., & Wang, R. (2018, March 14). Updated: The potential impact of short-term limited-duration policies on insurance coverage, premiums, and federal spending. Retrieved from https://www.urban.org/sites/default/files/publication/96781/2001727_updated_finalized.pdf

[9] U.S. Office of the Assistant Secretary for Planning and Evaluation (ASPE). (2017, June 25). Individual market premiums, 2013 to 2017, by state. Retrieved from https://aspe.hhs.gov/ interactive/individual-market-premiums-2013-vs-2017-state#tab-631-2

[10] Snowbeck, C. (2017, November 14). Farmer cooperative health plans may rattle individual market in Minnesota. Star Tribune. Retrieved from http://www.startribune.com/farmer-cooperative-health-plans-may-rattle-individual-market-in-minnesota/457321193/

[11] Snowbeck, C.(2018, January 8). Farmer health plans draw 1,700 in Minnesota. Star Tribune. Retrieved from http://www.startribune.com/farmer-health-plans-draw-1-700-in-minnesota/468369493/

[12] Norris, L. (2018, June 20). Iowa health insurance marketplace: history and news of the state’s exchange. HealthInsurance.org [blog]. Retrieved from https://www.healthinsurance.org/iowa-state-health-insurance-exchange/#2019

[13] Jordon, S. (2018, April 3). Iowa Farm Bureau will sell health plans outside ‘Obamacare’ exchange. Omaha World Herald. Retrieved from http://www.omaha.com/livewellnebraska/consumer/iowa-farm-bureau-will-sell-health-plans-outside-obamacare-exchange/article_0ca98a68-9b97-54e6-a39d-81c282570442.html

[14] Henry J. Kaiser Family Foundation. (2018). Total Marketplace Enrollment [Data set]. Retrieved from https://www.kff.org/health-reform/state-indicator/total-marketplace-enrollment/?currentTimeframe=0

[15] Livingston, S. (2018, February 20). Trump administration to expand access to short-term insurance without ACA protections. Modern Healthcare. Retrieved from http://www.modernhealthcare.com/article/20180220/NEWS/180229999

[16] Keith, K. (2019, July 20).Court Upholds Rule on Short-Term Plans. Health Affairs [blog]. Retrieved from https://www.healthaffairs.org/do/10.1377/hblog20190720.616648/full/

[17] eHealth. Demand for short-term health insurance has steadily grown since implementation of the ACA [press release]. 2018. https://news.ehealthinsurance.com/news/demand-for-short-term-health-insurance-has-steadily-grown-since-implementation-of-the-aca. Published March 7, 2018. Accessed August 8, 2018.

[18] Keith, K. (2018, May 21). CMS actuary finds risk of short-term plans to be higher than estimates in proposed rule. Health Affairs [blog]. Retrieved from https://www.healthaffairs.org/do/10.1377/ hblog20180521.682815/full/

[19] Rao, P., Nowak, S.A., & Eibner, C. (2018, June 5). What is the impact on enrollment and premiums if the duration of short-term health insurance plans is increased? Retrieved from https://www.commonwealthfund.org/publications/fund-reports/2018/jun/what-impact-enrollment-and-premiums-if-duration-short-term?redirect_source=/publications/fund-reports/2018/jun/short-term-plans-enrollment

[20 Corlette, S. (2018, August 1). Short-term, limited duration insurance Final Rule: Summary and state options.Retrieved from https://www.shvs.org/short-term-limited-duration-insurance-final-rule-summary-and-state-options/

[21] Blewett, L.A., Ziegenfuss, J., & Davern, M.E. (2008). Local access to care programs (LACPs): new developments in the access to care for the uninsured. Milbank Quarterly, 86(3), 459-79. doi:10.111/j.1468-0009.2008.00529.

[22] Georgetown Center for Health Insurance Reforms (CHIR) Faculty. (2013, July 28). What do you know about health care sharing ministries? CHIR [blog]. Retrieved from http://chirblog.org/what-do-you-know-about-health-care-sharing-ministries/

[23] Alliance of Health Care Sharing Ministries. (n.d.). Purpose. Retrieved from http://www.healthcaresharing.org/about-us/#purpose. Accessed August 8, 2018.

[24] Santhanam, L. (2018, January 16). 1 million Americans pool money in religious ministries to pay for health care. Retrieved from https://www.pbs.org/newshour/health/1-million-americans-pool-money-in-religious-ministries-to-pay-for-health-care