February 05, 2016

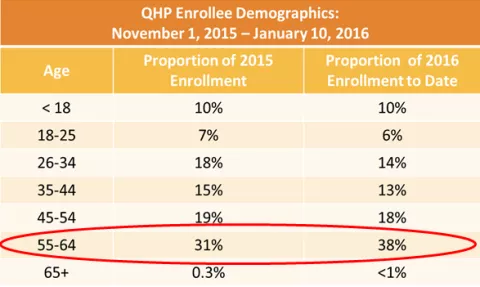

Two years ago I authored a blog on early retirees flooding the health insurance marketplaces. While there wasn’t exactly a flood, there was an increase from 2015 to 2016 in the proportion of older enrollees (ages 55-64) in coverage obtained through MNsure.

Image

Source: MNsure Board Meeting on January 13, 2016. Slides available at: https://www.mnsure.org/images/bd-2016-01-13-deck.pdf

There are a number of factors that may explain the increase in the proportion of MNsure enrollment attributable to the population aged 55-64.

- People aged 55-64 are more likely to experience chronic health conditions than are younger adults and children. As a result, people aged 55-64 are more likely to need health insurance coverage and less likely to forego coverage in the absence of an employer offer.

- Individuals aged 55-64 in need of individual coverage have more incentive to seek coverage through MNsure because of its offer of premium assistance. Under the ACA, premiums can no longer be tied to gender or pre-existing conditions, but premiums can still vary by age. As a result, 55-64 year olds can face premiums that are as much as three times greater than the premiums for the youngest enrollees.

For example, the lowest cost bronze plan with a $6,450 deductible is $140 a month for a 25-year-old nonsmoker compared to $380 per month for a 60-year-old nonsmoker. The estimated premium subsidy (using the MNsure plan comparison tools) for a 60-year-old with an annual income of $29,425 (250% of the 2015 Federal Poverty Guideline), would amount to $299 per month. The premium assistance available through the Marketplace would lower the monthly premium to $81 per month.

- Employers are discontinuing their early retiree benefits and directing them to the Marketplace for coverage. Based on the Kaiser Family Foundation Employer Health Benefits Survey, the percentage of large employers providing workers with retirement health coverage has dropped from 66 percent in 1988 to 23 percent in 2015. Early retiree benefits have been decreasing since before the implementation of the ACA, but ACA provisions such as premium assistance through the Marketplace have accelerated the trend. About a quarter (26%) of large employers still offering retiree benefits are considering changes to their retiree coverage due to the new ACA insurance marketplaces.

For example, Minnesota-based 3M no longer offered early retirement benefits starting in 2015. More recently, the Star Tribune reported that Target would be discontinuing early retiree health care benefits beginning on April 1, 2016. Target suggested to employees the company is phasing out early retiree benefits “because there are more economical alternatives through Obamacare.”

- One reason employers are discontinuing early retirement benefits is due to the expiration of the Early Retiree Reinsurance Program established under the ACA. This program provided financial assistance to employers who maintained their early retirement programs during the first years of implementation of the ACA, making available an 80 percent subsidy for claims between $15,000 and $90,000 for those aged 55 and older that were ineligible for Medicare. The subsidy was also available for spouses, surviving spouses, and dependents’ claims. In all, the Department of Health and Human Services provided $5 billion in funding to employers between 2010 and 2011. Employers that received support included cities, counties, states and several large Minnesota companies. Minnesota received $67 million and ranked 17 out of the 50 states (and D.C.) participating in the program. Some of the top employer recipients included the following:

Image

Source: Centers for Medicare & Medicaid Services. 2014. “Early retirement reinsurance program: reimbursements as of June 25, 2014.”

With the loss of this significant federal funding, employers have less incentive to maintain early retirement benefits.

MNsure has proven to be an important source of coverage for adults aged 55-64 and as the Baby Boomers age; they will continue to be a growing population to support.