With the recent focus on health insurance coverage purchased through Affordable Care Act marketplaces, it is easy to forget that the majority of individuals are enrolled in health insurance through their employer (56% in 2015).[1] This blog is the second in a series that highlights the experiences of individuals enrolled in private sector employer-sponsored insurance. It uses data from the Medical Expenditure Panel Survey-Insurance Component (MEPS-IC) recently collected by the Agency for Healthcare Research and Quality (AHRQ).

What are premiums?

Premiums are the amount of money paid every month for health insurance coverage. In the context of employer-sponsored insurance, employers typically pay 70%–80% of an employee’s premium, and the employee covers the remaining cost. Employer contributions to premiums are nontaxable income, and the employee’s share comes out of pre-tax income. In addition to premiums, employees may also have to pay for other health care costs like a deductible, copayments, and coinsurance.

ESI premiums have been increasing steadily, but growth has slowed.

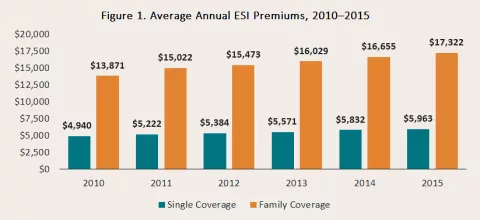

Premiums for employer-sponsored insurance have been increasing over time. In 2015, the average total premium for single coverage was $5,963, an increase of more than $1,000 since 2010 (Figure 1). The average total family premium was $17,322 in 2015, an increase of almost $3,500 over the same period.

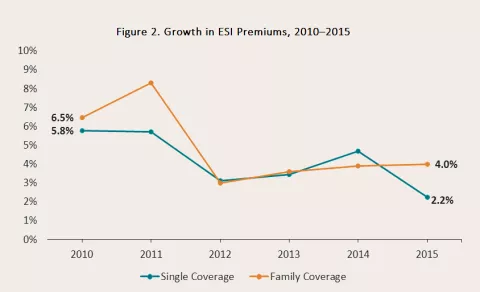

Since 2010, single-coverage premiums have grown at an average rate of 4.3% per year, while family-coverage premiums have grown at an average rate of 4.9% per year. However, since 2012, premiums have been growing at a slower rate. Between 2014 and 2015, premiums for single coverage rose at a relatively modest rate of 2.2%, and family premiums rose 4.0% (Figure 2).

ESI premium levels and growth varied across states in 2015.

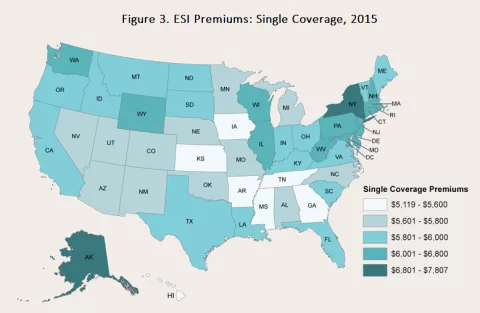

In 2015, the average total premium for single coverage ranged from $5,119 in Arkansas to $7,807 in Alaska (this gap was mirrored in the family plan premiums, which ranged from $14,218 in Arkansas to $21,089 in Alaska).

Premium growth also varied by state; growth in single-coverage ESI premiums ranged from a 5.2% decrease in premiums in Vermont to a 16.9% increase in Idaho in 2015. The map in Figure 3 shows average state-level ESI premiums for a single plan in 2015.

National premium increases were driven by relatively few states in 2015.

In total, only six states had a statistically significant increase in single-level ESI premiums between 2014 and 2015 (Figure 4). Among those, three states--Idaho, Virginia, and Alaska--had double-digit increases.

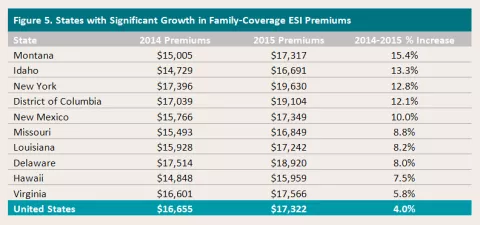

Only ten states had a statistically significant increase in family-level ESI premiums between 2014 and 2015 (Figure 5). Among those, half had double-digit premium increases.

Discussion

While moderation in premium growth in the ESI market at the national level is certainly good news for employers and employees alike, it masks significant variation in both the size of premiums across the states as well as difference in the rate of premium growth. For example, while Alaska had the lowest ESI single-premium rates in 2015, it also had the third highest premium increase in single premiums between 2014 and 2015. In addition, it is important to remember that premiums are only one component of the cost of insurance. While premium rates have been moderating since 2012, the number of workers enrolled in high-deductible plans has been on the rise. In 2015, almost 40% of private sector workers were enrolled in a high-deductible plan through their employer. This represents an almost threefold increase between 2008 and 2015. This has important implications for the total cost that employees are paying for their health care.

[1] Barnett, J.C., & Vornovitsky, M. September 13, 2016. “Health Insurance Coverage in the United States: 2015.” Current Population Reports. Washington, DC: U.S. Census Bureau. Available at http://www.census.gov/content/dam/Census/library/publications/2016/demo/p60-257.pdf